Digital Currencies Are Not Behaving the Way You Would Expect

Smart Contract Platforms Are Being Used More, But Earning Less

DeFi Lending Had a Strong Run and Is in a Healthy Place Despite the Recent Dip

Decentralised Trading Is Growing, But Margins Are Thin

CEX Tokens Are One to Watch as Regulations Get Clearer

What All of This Is Actually Telling Us

Most people look at crypto prices the same way they look at the weather. They see a number, decide if things are good or bad, and move on. But just like the weather only tells you what today looks like, a price only tells you what the market is right now. It says nothing about whether these networks are actually being used, whether they are making real money, or whether the growth behind them will last.

Think of it like a restaurant. A long line outside tells you the place is popular. But it says nothing about whether the restaurant is actually profitable, or whether it will be around next year. For that, you need to look at the actual numbers.

Crypto works the same way. The prices you see every day are the line outside. We went behind those prices across five major categories: digital currencies, smart contract platforms, DeFi lending, decentralised exchanges, and centralised exchange tokens, and looked at what their underlying numbers are saying.

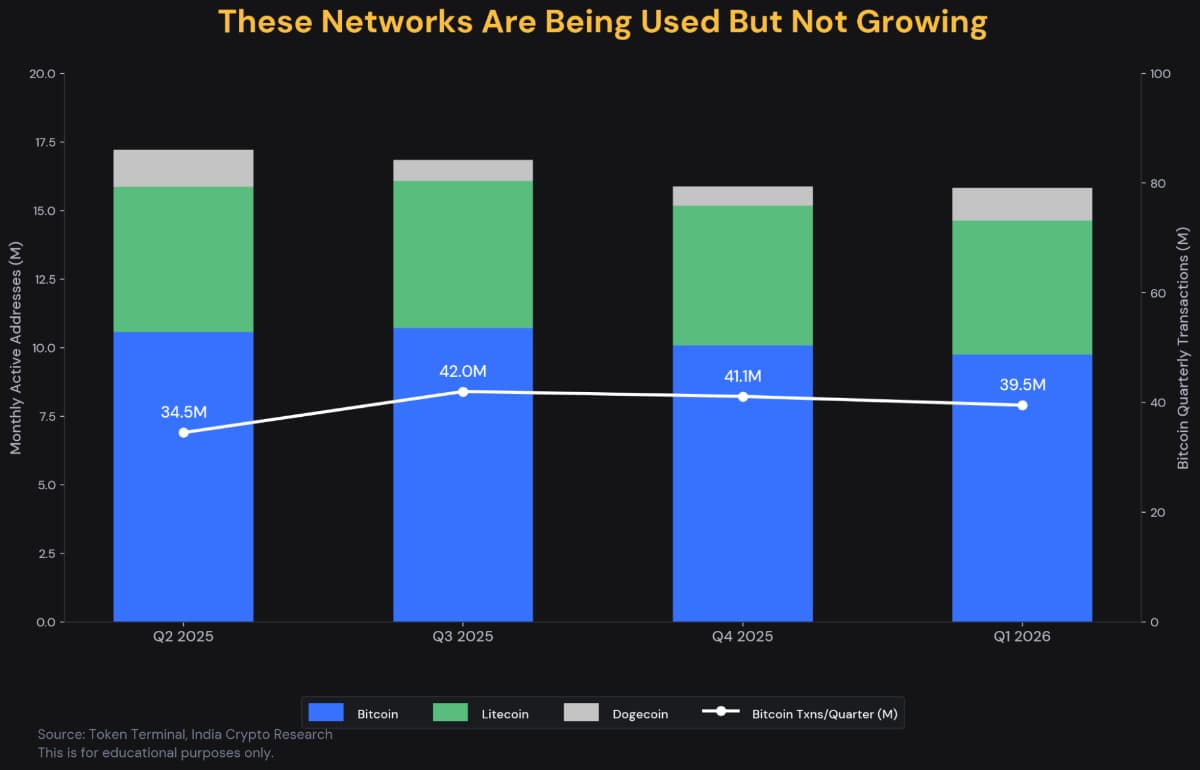

Digital currencies are the original version of crypto. The idea was simple. Send money directly to someone, anywhere, without going through a bank. Bitcoin was built for this.

But Bitcoin today is not really used the way it was designed. Most people buy it and hold it rather than spend it. It is not quite a store of value like gold either; its price is still heavily driven by sentiment, macro conditions, and institutional flows. It sits somewhere in the middle, and the data reflects that. If you are one of the many Indian investors buying and holding these assets, remember that crypto gains are taxed at a flat 30 percent and must be reported, so plan to file your ITR and declare them correctly.

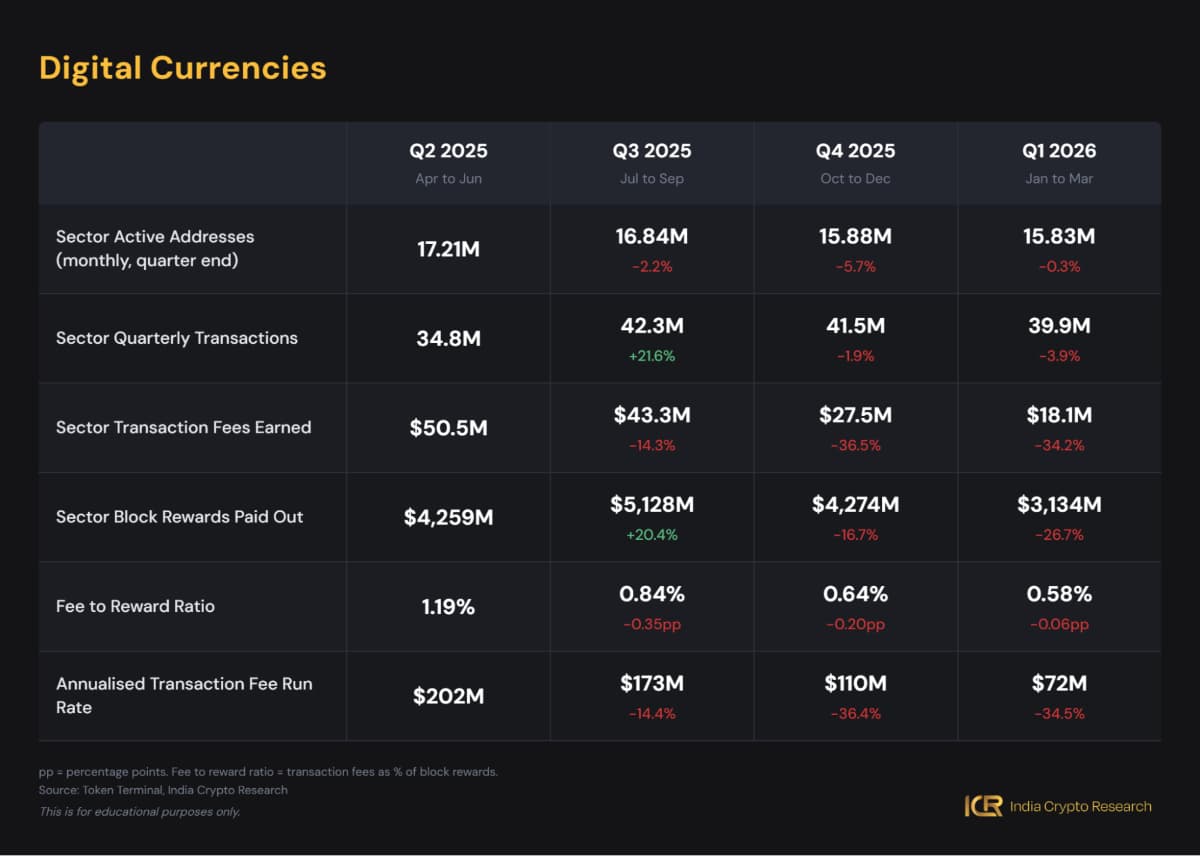

The number of wallets actively transacting on these networks has come down slightly but steadily, from 17.21 million to 15.83 million by Q1 2026. Not a collapse, but not growing either.

The bigger question is around miner economics. Miners keep these networks secure and get paid in two ways: transaction fees from users, and block rewards, which are newly created coins. Block rewards are around $3 to $5 billion per quarter. Transaction fees fell from $50 million in Q2 2025 to just $18 million by Q1 2026.

That gap is getting wider every quarter. Bitcoin halves its block rewards roughly every four years, and the expectation was always that fee income would grow to fill that gap. That has not happened yet.

Smart contract platforms are the infrastructure that everything else in crypto runs on. When you use a DeFi app, trade on a decentralised exchange, or hold a token, there is a blockchain underneath making it all possible. This sector earns fees every time someone uses it, similar to how a payment network charges a small amount per transaction.

Looking at the sector as a whole, total fees came in at $4.82 billion between Q2 2025 and Q1 2026. But nearly 68% of that came from a single chain. Tron, a blockchain most people outside of Asia have not heard of, quietly earned $3.29 billion in fees over this period. It is not doing anything flashy. Almost all of it comes from people using USDT to transfer money across borders in Asia, Africa, and Latin America. It is boring, consistent, and has real-world usage.

Ethereum, which most people associate with crypto applications, contributed just 7% of sector fees. Its fees fell sharply, not because fewer people are using Ethereum, but because it deliberately made transactions cheaper by routing activity to secondary networks built on top of it. More activity, lower fees per transaction.

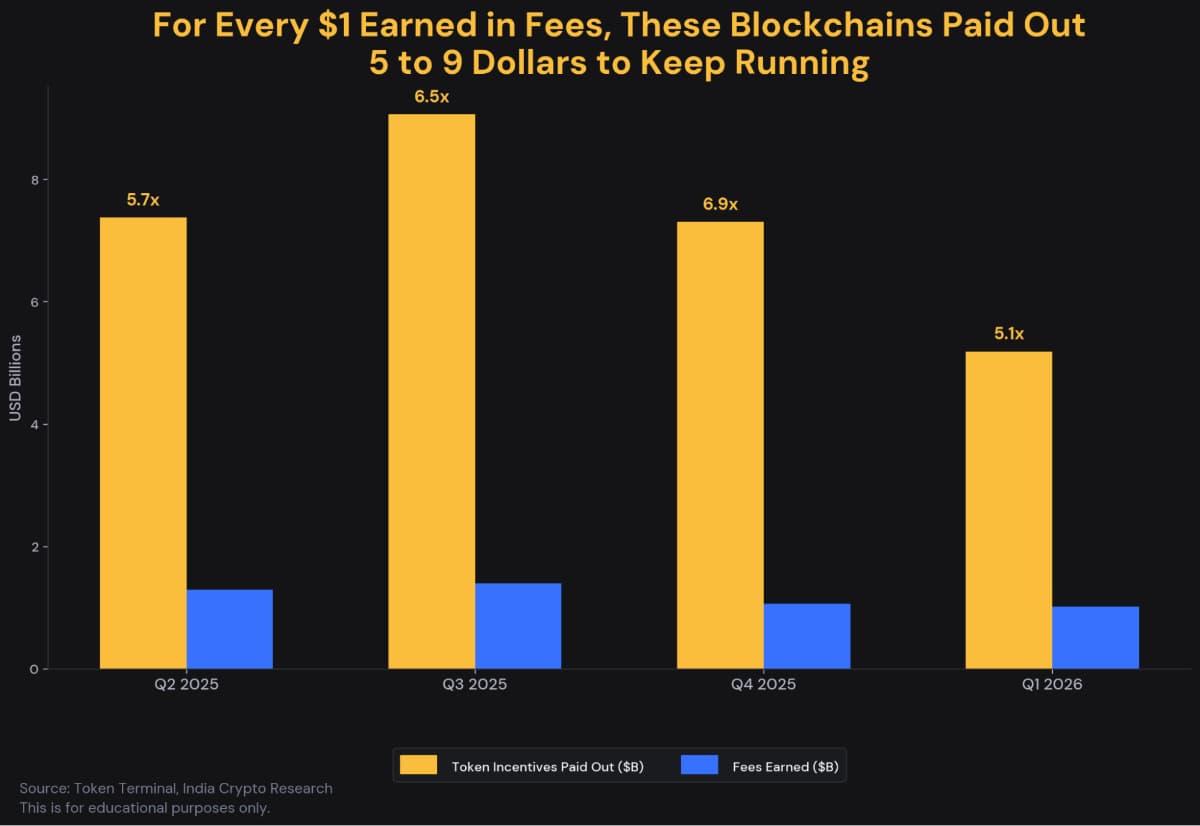

The bigger concern for the sector is the chart you see below. Blockchains pay the people who run their networks in newly created tokens. Think of it as a salary paid in company stock. In Q4 2025, the sector paid out nearly seven dollars in these token rewards for every one dollar it earned in actual fees. That ratio improved to five dollars in Q1 2026, which is a step in the right direction, but the fees these networks earn from actual usage are nowhere near the ideal level.

Imagine a bank where there are no forms to fill out, no credit checks, and no relationship manager to call. You deposit crypto, someone else borrows it, and the interest is handled automatically by code. That is DeFi lending in a sentence.

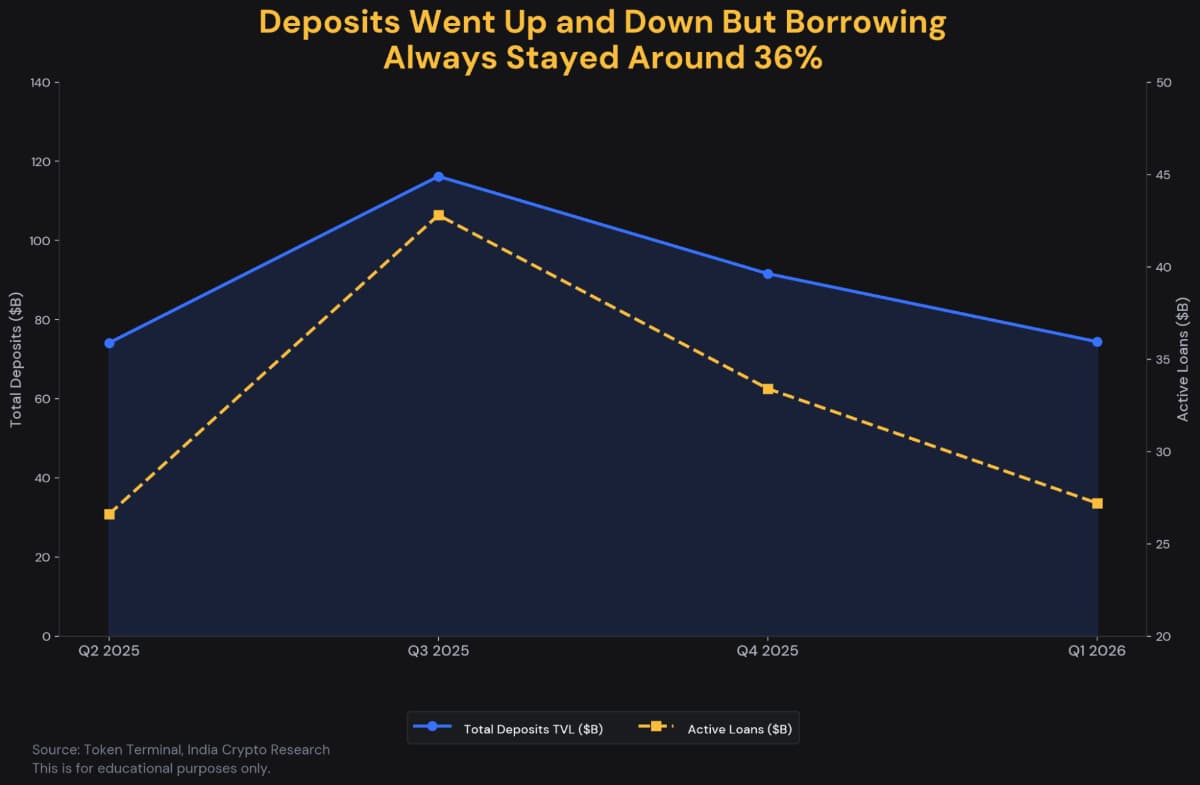

Total deposits across DeFi lending protocols swung dramatically over the past four quarters. They started at $74.1 billion, surged to $116.2 billion at the Q3 2025 peak, and then came back down to $74.4 billion by Q1 2026 as markets corrected. Almost the entire gain was given back. But even at this post-correction level, deposits are sitting higher than the peak of the entire 2021 bull market, which topped out at around $51 billion. What looks like a retreat is actually a very healthy floor.

But here is what did not change. The share of deposits being actively borrowed stayed at roughly 36% in every single quarter. When markets were booming, and deposits nearly doubled, borrowing grew with them. When markets fell, and deposits shrank, borrowing pulled back just as proportionately. That kind of consistency tells you the demand to borrow on these platforms is structural, not just speculation riding a bull market.

Aave accounts for roughly 55% of all deposits in this sector and an even higher share of active loans at around 61%. Think of it as the HDFC of DeFi lending, dominant, well-established, and hard to displace. In April 2025, it started buying back its own tokens using the fees it earns, which only makes sense when a protocol has more money coming in than it needs to spend. Morpho, a newer entrant, has grown its loan book by over 100% in a year by offering better rates through a smarter matching model.

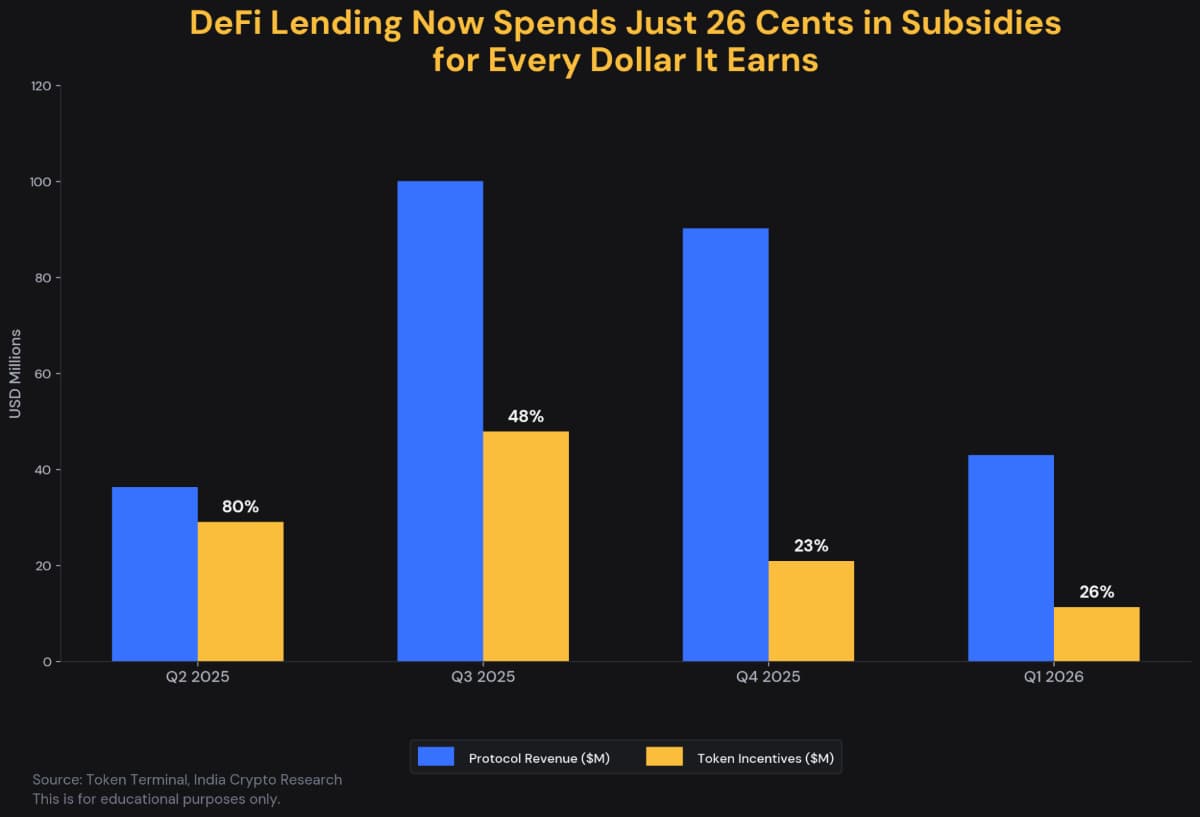

Perhaps the most encouraging sign is how much less these protocols are spending to attract users. Earlier, they used to hand out token rewards aggressively to pull deposits in, spending 80 cents for every dollar they earned. That ratio is now down to around 26 cents. The sector is becoming genuinely self-sustaining.

A decentralised exchange lets you trade crypto directly from your wallet. No company holding your funds, no account to create. The trade happens automatically through code.

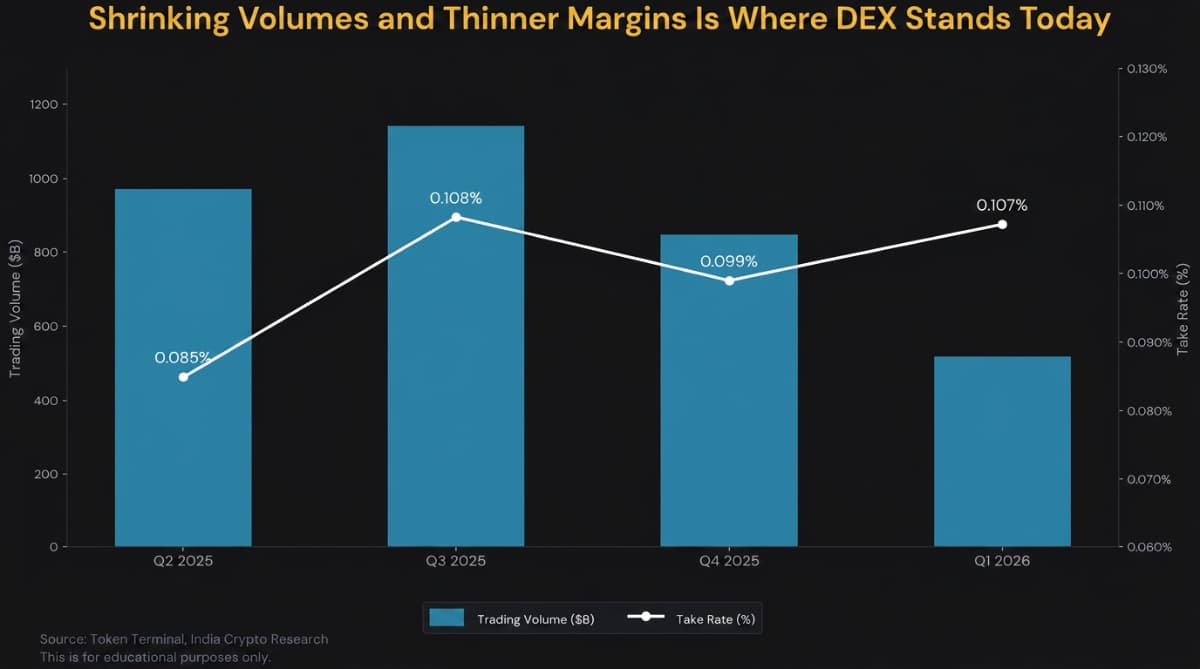

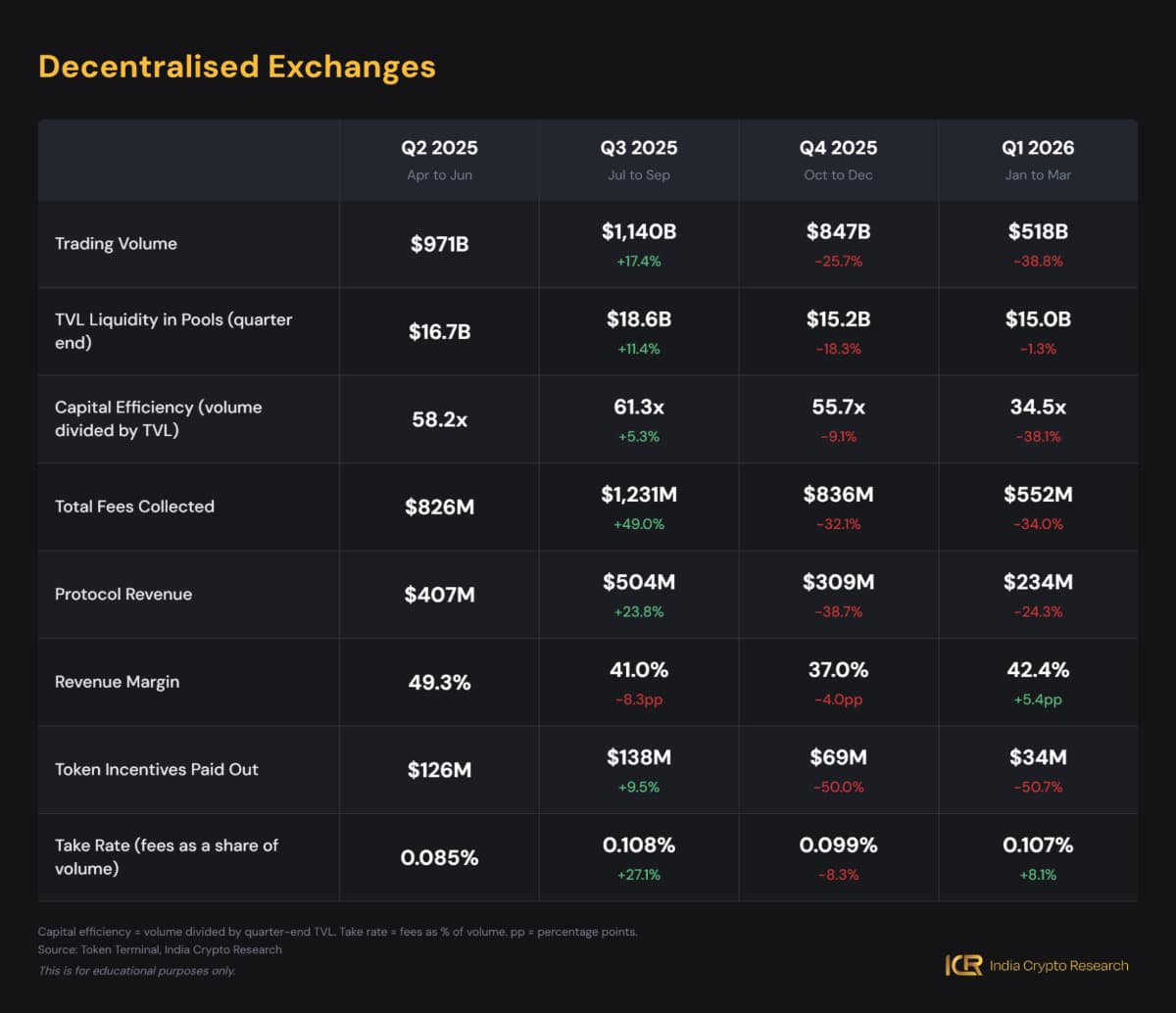

One of the clearest ways to measure how healthy a DEX is is to look at trading volume. Because everything else, fees, protocol revenue, liquidity, all follow from it. The sector did $3.47 trillion in volume across the four quarters we tracked. PancakeSwap and Uniswap alone accounted for over 65% of that.

But here is the thing. Volume does not automatically mean income. Think of a shop getting more customers but offering bigger and bigger discounts to attract them. The footfall looks great. The margins do not. The fee collected per dollar traded has stayed compressed throughout, sitting between 0.085% and 0.108% across all four quarters. More trading, but less earned per trade.

The bright spot is in derivatives. A derivative is simply a contract that lets you bet on whether a price will go up or down, without actually owning the asset. Decentralised platforms handling this type of trading saw their share of the total derivatives market jump from 2.5% to 7.8% through 2025. That growth is driven by actual demand, not subsidies.

Q1 2026 saw a sharp 38.8% drop in spot trading volume. The question heading into Q2 is whether that is the market pulling back temporarily, or something more structural starting to show.

Every major centralised exchange has its own token. Binance has BNB, OKX has OKB, and Crypto.com has CRO. These are not just currencies. They give holders fee discounts, voting rights, and, in a way, exposure to how well the exchange is doing. Exchanges also regularly burn these tokens, meaning they destroy a portion of the supply using their profits. Less supply over time tends to support the price.

BNB is the dominant one with a market cap of around $84 billion, making it one of the top five cryptocurrencies in the world. OKB and CRO are significantly smaller, in the $2 to $4 billion range.

On regulation, two things happened in 2025 that matter for this sector. The GENIUS Act was signed into law in July, the first US federal law for crypto, covering stablecoins. The CLARITY Act, which would define how all digital assets are regulated, passed the House in July 2025 and is still working through the Senate. For CEX tokens, regulatory clarity is everything. When the rules are clear, institutions participate more freely, volumes go up, and the token burns become more meaningful.

DeFi lending is the strongest sector by fundamentals. Deposits are high, the loan to deposit ratio has held steady even through a price correction, and protocols are now earning real revenue without leaning on subsidies the way they used to. The direction is clearly improving.

Digital currencies are stable from a usage standpoint, but the fee-to-reward gap is the one number that needs watching. Miners today earn almost nothing from transaction fees relative to what they get in block rewards. As those rewards halve over time, fee growth needs to pick up. It has not started yet.

Smart contract platforms paid out less in incentives in Q1 2026 than they did in Q4 2025, which brought the subsidy ratio down from 6.9x to 5.1x. That is an improvement, but it came from spending less, not earning more. Real progress would look like fee growth.

DEX had a sharp volume drop in Q1 2026. The take rate has stayed compressed. The bright spot is perpetual futures trading, where decentralised platforms are genuinely taking share from centralised ones. That is the part of this sector worth watching.

CEX tokens are tied closely to regulatory progress. The GENIUS Act is done. The CLARITY Act is the next domino. If it passes, the operating environment for exchanges gets significantly clearer, which tends to flow directly into exchange activity and token value.

Tracking fundamentals across all these categories is something most people do not have the time to do. The India Crypto Research Score was built for exactly this. It looks at the key fundamental metrics of a protocol, fees, revenue, active users, incentives and more, and gives it a score that reflects how healthy it actually is.

India Crypto Research operates independently. The information presented herein is intended solely for educational and informational purposes and should not be construed as financial advice. Before making any financial decisions, it's essential to undertake your own thorough research and analysis. If you're uncertain about any financial matters, we strongly recommend seeking guidance from an impartial financial advisor.