Loading Data ...

Aave is the largest decentralised lending protocol in DeFi. It lets users deposit crypto assets to earn interest, or borrow against their holdings without selling them, all without a bank or broker in the middle. The protocol holds over $25 billion in deposits across multiple chains as of 2026, making it the dominant player in on-chain lending by a significant margin. AAVE, its native token, is used for governance, staking in the Safety Module, and protocol incentives.

Stani Kulechov founded the project as ETHLend in November 2017 while studying law at the University of Helsinki. The ICO raised around $16.2 million. The original concept was peer-to-peer collateralised loans on Ethereum, but the model evolved quickly.

In 2018, the project rebranded to Aave, the Finnish word for ghost, a nod to the idea of invisible, intermediary-free finance. The pooled liquidity model replaced the peer-to-peer structure, and the protocol has been iterating ever since. Aave V1 launched in January 2020, V2 in December 2020, V3 in March 2022, and V4 in March 2026.

Aave invented flash loans in 2020. The idea sounds impossible at first: borrow millions of dollars worth of crypto with no collateral. But there is a catch that makes it work. The loan must be borrowed and repaid in a single Ethereum transaction, which typically takes about 13 seconds.

If repayment does not happen, the entire transaction reverts as if it never occurred. The lender never loses anything because the loan unwinds. This makes flash loans risk-free from the protocol's perspective, and useful for arbitrage, collateral swaps, liquidations, and refinancing across DeFi protocols.

GHO is Aave's native stablecoin, launched in July 2023. Users mint GHO by locking collateral in Aave V3 markets, similar to how MakerDAO's DAI works. The supply grew from $35 million at launch to $527 million by the end of 2025, making it one of the fastest-growing decentralised stablecoins in DeFi.

Aavenomics refers to a major governance update passed in 2025 that restructured the AAVE token's economics. It introduced a $50 million annual buyback funded by protocol revenue, and a new reward token called anti-GHO for AAVE stakers. The update was designed to make holding and staking AAVE more directly tied to the protocol's performance.

Aave started as ETHLend in 2017, a peer-to-peer lending idea that raised $16.2 million in an ICO. The rebrand to Aave came in 2018 alongside a fundamental shift in the model: from matching individual lenders and borrowers to pooling liquidity and letting rates adjust algorithmically.

V1 launched in January 2020, introducing aTokens that accrue interest in real time. V2 followed in December 2020 with flash loans, credit delegation, and gas optimisations. V3 expanded across multiple chains in 2022: Polygon, Avalanche, Arbitrum, Optimism, and Base. GHO launched in 2023. By 2024, Aave had become the largest DeFi lending platform by deposits. In 2025, the Aavenomics update restructured token economics, and Aave Labs launched Horizon, a product for institutional stablecoin borrowing against tokenised real-world assets. V4 launched on the Ethereum mainnet in March 2026.

You deposit an asset into Aave's liquidity pool and receive an aToken in return, which represents your position and accrues interest automatically. Borrowers pay interest to access the pool, and that interest flows to suppliers. Rates adjust algorithmically based on utilisation: the more of the pool that is borrowed, the higher the rate. You can withdraw your deposit at any time as long as there is liquidity in the pool.

Using Aave is not banned in India. It is a decentralised protocol accessed through a web interface, not a regulated financial product. That said, any yield earned or gains made through Aave are subject to Indian tax law. Gains are taxed at a flat 30% plus cess, and any transfer of crypto assets attracts 1% TDS. The regulatory framework around DeFi in India is still evolving.

Aave accepts a wide range of collateral depending on the market and chain. On the Ethereum mainnet, commonly used collateral includes ETH, wBTC, stETH, USDC, and USDT. Each asset has a loan-to-value ratio that determines how much you can borrow against it. Higher quality assets like ETH and stETH typically have LTV ratios of 75-80%. Riskier or less liquid assets have lower LTVs or are listed as non-collateral assets.

Aave is a decentralised protocol, so there is no account or KYC required. You connect an Ethereum-compatible wallet like MetaMask to app.aave.com and interact directly with the protocol. To supply or borrow, you need the asset in your wallet plus some ETH for gas fees. Layer 2 networks like Arbitrum and Base significantly reduce gas costs compared to the Ethereum mainnet.

Aave has been running since 2020 and has processed hundreds of billions in lending volume without a major protocol exploit. It has undergone extensive auditing and has a Safety Module where AAVE holders stake tokens as a backstop against shortfall events. That said, smart contract risk is real. No DeFi protocol is completely risk-free. Liquidation risk is also relevant if your collateral value falls below the required threshold.

Yield earned on Aave, whether from supplying assets or staking AAVE in the Safety Module, is likely treated as income from other sources and taxed at your applicable income tax slab rate. Any gains from selling aTokens or AAVE are subject to the flat 30% crypto gains tax plus cess. The 1% TDS applies to transfers through Indian exchanges, though direct wallet interactions with Aave may not trigger TDS at source.

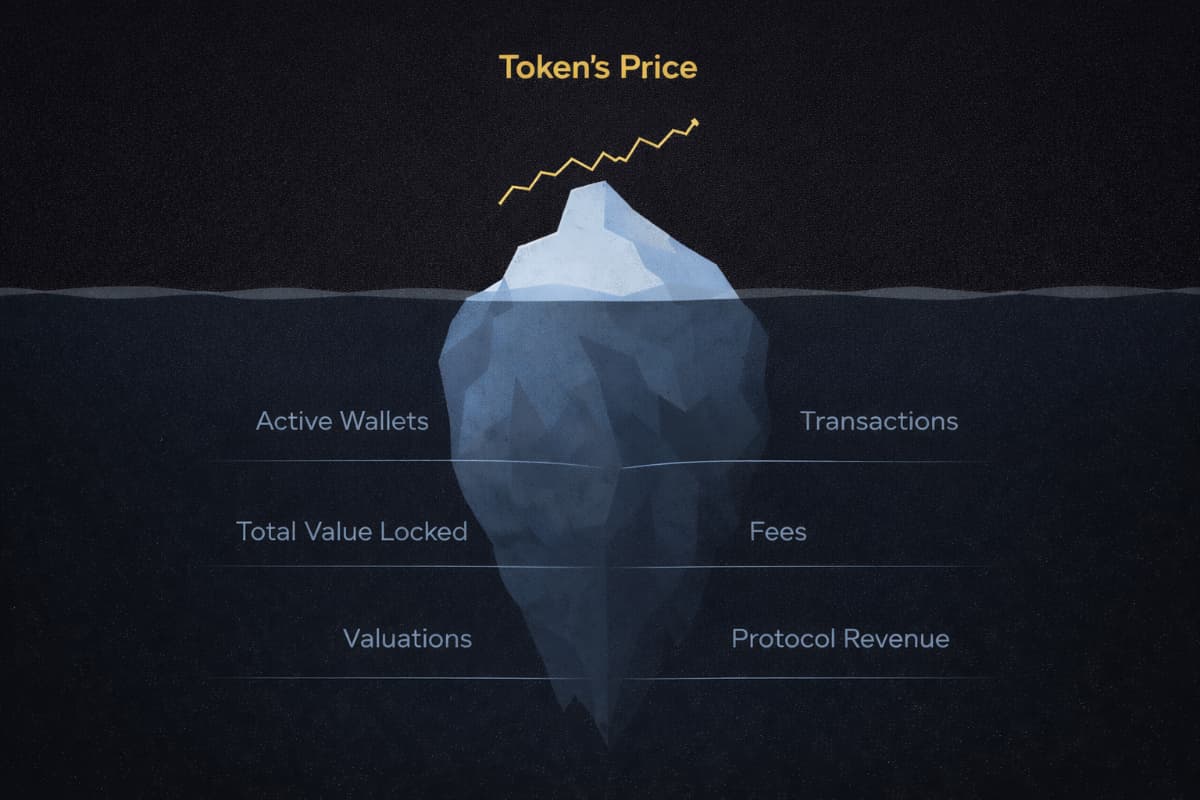

The key metrics are total value locked across all markets and chains, protocol revenue, active borrowers, GHO supply and peg stability, AAVE token buyback volume, and Safety Module staking participation. ICR Score combines all of these into a single proprietary score, giving you one place to assess Aave's fundamental health.