First, What Does Tokenisation Actually Look Like?

Why BlackRock Is Moving Its Safest Product to Crypto Rails

Why Retail Investors Miss the Biggest Wealth Creation of Every Decade

You Can Spread Your Stock Portfolio Across 50 Companies. Real Estate Does Not Work Like That.

Gold Is Becoming More Than Just a Store of Value

Three Major Shifts Are Happening at the Same Time

Every major asset class you can think of, bonds, stocks, real estate, and gold, is being rebuilt on a new kind of infrastructure. Ownership is starting to look more flexible, liquid, and programmable than before. The asset itself doesn't change. What changes is how small a piece you can own, how fast you can move it, what hours it trades, and what you can do with it after you buy it.

The tokenised real-world asset market crossed $19 billion in early 2026, more than tripling over the past 15 months. The numbers will get much bigger. What follows is a closer look at how these four asset classes are being rebuilt, and why the underlying financial system may look very different over the next decade.

Picture a regular investment app. You sign up, complete KYC, and deposit money. A tokenised product works the same way at the surface. The difference is what you receive. Instead of a mutual fund unit sitting in a demat account, you get a token on a blockchain. The token says you own one unit of a US Treasury fund, or 0.1 ounces of gold, or 0.002% of a Singapore office building. The underlying asset still exists in a real vault or custody account. The token is a faster, more flexible version of a share certificate. You can move it between apps, hold it in your own wallet, pledge it as collateral to borrow against, or trade it at 2 am on a Sunday.

The global bond market is $145 trillion against $127 trillion for global equities. Bonds are bigger than stocks. Yet for most retail investors, bonds remain an afterthought. Most Indians put their money in FDs and stop there. The reason is partly cultural and partly structural. Bonds were built for institutions, and the experience of buying one as a retail investor still feels that way.

The current bond market has real friction. Secondary market liquidity can be weak, especially for retail investors. Selling before maturity often means taking a price hit, and in less liquid bonds, even finding a buyer can be difficult. Cross-border access is painful: an Indian wanting US Treasury exposure today goes through LRS, opens a foreign brokerage, converts currency, and files Schedule FA in their ITR. Bonds mostly sit idle. You earn the coupon, but the asset itself remains relatively passive inside the traditional system.

Tokenisation changes this. A tokenised bond trades 24/7 on-chain. The same bond can earn its coupon while being pledged as collateral in DeFi, double-using the same capital. BlackRock's BUIDL fund, which holds short-dated US Treasuries on Ethereum, crossed $2 billion in AUM within 24 months of launch. JPMorgan, Fidelity, and Franklin Templeton have similar products live. Indian retail cannot legally access these today. IFSCA's GIFT City sandbox is the most likely first opening.

Global public equity is $127 trillion. Private equity is another $5.3 trillion in a parallel universe most retail never sees. The biggest companies of this decade, SpaceX, OpenAI, Stripe, and Anthropic, have all created hundreds of billions in value while staying private. Retail captures very little of it.

The friction is different in each bucket. For public equity, Indian retail can technically access US stocks through LRS, but with 20% TCS above ₹10 lakh remittance, currency conversion fees at both legs, and tax filing complications. For private equity, the barrier is structural: Indian AIFs require ₹1 crore minimums and lock capital up for 7-10 years with no secondary exit. US private equity requires accredited investor status ($1M+ net worth). The 95% of investors who would want exposure are mathematically excluded.

Tokenisation cracks both open. Robinhood EU offers tokenised US stocks with €1 minimums and 24/5 trading. Kraken and Backed Finance offer regulated tokenised equity products backed by underlying shares or equivalent structures. More interestingly, platforms like Republic and Injective have started offering tokenised exposure linked to companies like SpaceX, OpenAI, and Anthropic, with minimums as low as around $50-$100, depending on the structure. In some cases, these products do not represent direct equity ownership, but they do give retail investors economic exposure to private companies that were historically inaccessible outside venture capital and institutional circles.

When Robinhood launched OpenAI tokens in June 2025, OpenAI publicly disputed that they were equity. They were SPV-based exposure tokens, not actual shares. The economic exposure was real, but the legal ownership was not. Tokens can mean different things. Investors need to know which one they hold.

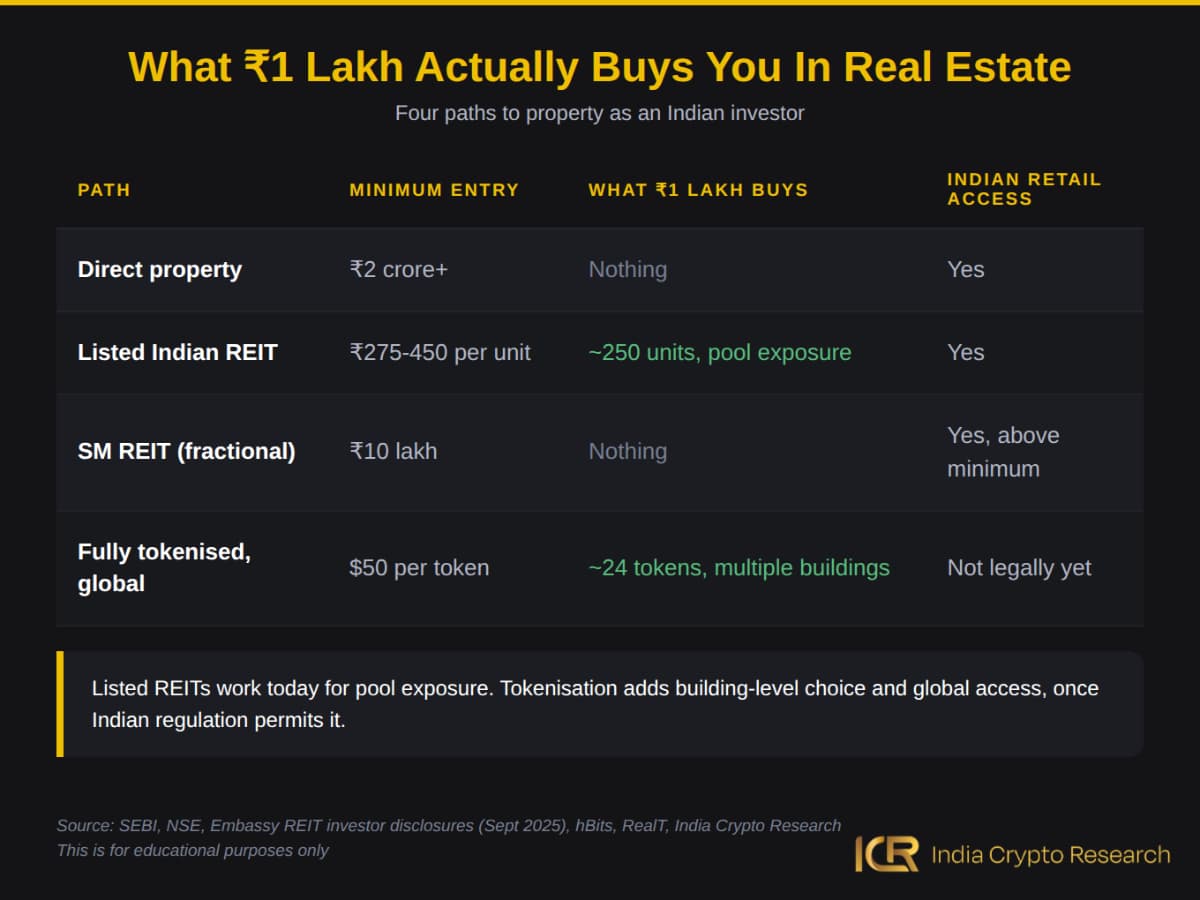

Global real estate is $393 trillion, the largest asset class on the planet. Indian commercial property alone is around ₹4 lakh crore. For most Indian investors, real estate is the least diversified part of their portfolio, and they don't really have a choice. The asset comes in big units.

A Grade A office building in BKC trades at ₹500-1,500 crore. A residential flat in any tier-1 Indian city starts at ₹2 crore. Selling either takes 6-12 months. Stamp duty and brokerage eat 7-9% of the transaction value. The math means if you have ₹1 crore to invest in property, you buy one mid-tier asset in one location. Diversification across cities, asset types, or countries is mathematically impossible at retail scale.

Indian retail does have one path that already works. Listed REITs like Embassy, Mindspace, Brookfield, and Nexus trade on the NSE at ₹275-450 per unit. A ₹1 lakh investment gets you exposure to a portfolio of commercial buildings across multiple cities. They yield 6-8% and trade like stocks. The catch is you don't get to pick which building. You buy the whole pool.

Tokenisation adds two things on top. Building-level choice, where you decide which specific property you want exposure to. And cross-border access, where you can hold a slice of a Singapore office, a Dubai retail mall, and a Mumbai industrial park in one wallet. SEBI's Small and Medium REIT framework, finalised in 2024-25, is the closest Indian retail can come to this today. It allows fractional ownership of commercial property with a ₹10 lakh minimum. Full on-chain tokenisation of overseas property is a few years away, dependent on regulations and policies.

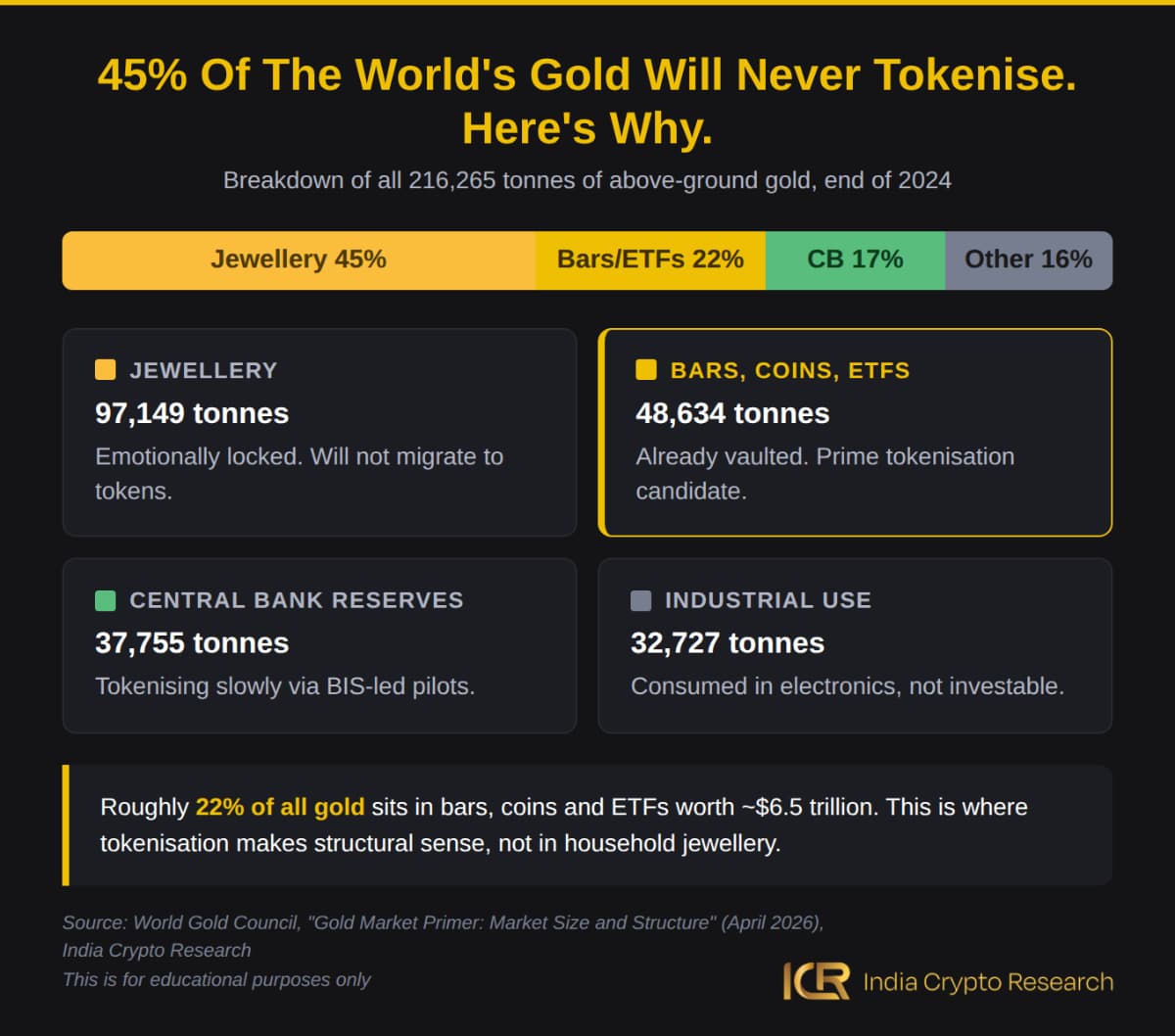

All gold ever mined sits at 216,000 tonnes, worth $29 trillion. Most pictures of gold show jewellery and coins. The reality is that huge portions of it sit in institutional vaults doing nothing. Gold ETFs alone hold 4,137 tonnes worth $615 billion as of April 2026. Investors hold paper. The underlying gold sits idle in London or New York vaults.

Gold ETF investors hold a gold claim that they cannot directly use. The gold cannot be moved between platforms in minutes. It cannot serve as collateral outside traditional banking. It earns zero yield. For most holders, gold historically generated no yield.

Tokenisation adds the missing functionality. PAXG and XAUT are tokens backed 1:1 by physical gold in audited London vaults, with minimums as low as 0.01 PAXG (around $42 at current gold prices). The new feature is yield. Platforms like Falcon Finance and Bitrue accept tokenised gold as collateral, paying 3-5% APR while the gold continues tracking spot prices. For an asset class that has earned no yield for most holders, this is genuinely new. The global tokenised gold market crossed $5.5 billion in Q1 2026, up 289% year on year, with spot trading volume of $90.7 billion in a single quarter exceeding all of 2025 combined.

Three things are happening globally at the same time.

The Indian regulatory picture is split. SEBI has built genuine frameworks like SM REITs and InvITs. IFSCA's GIFT City sandbox is the most likely first opening for tokenised securities. But tokenised assets still have no clear classification under Indian law. The 30% flat crypto tax may or may not apply. NRIs are already accessing these products. HNIs route through GIFT City. The infrastructure already exists. Regulation is now the main variable.

Crypto's first decade opened access to one new asset class. Tokenisation opens retail access to assets institutional finance has gatekept for a century. The Indian investor who studies this shift early will likely understand where financial infrastructure is heading before it becomes mainstream.

India Crypto Research operates independently. The information presented herein is intended solely for educational and informational purposes and should not be construed as financial advice. Before making any financial decisions, it's essential to undertake your own thorough research and analysis. If you're uncertain about any financial matters, we strongly recommend seeking guidance from an impartial financial advisor.