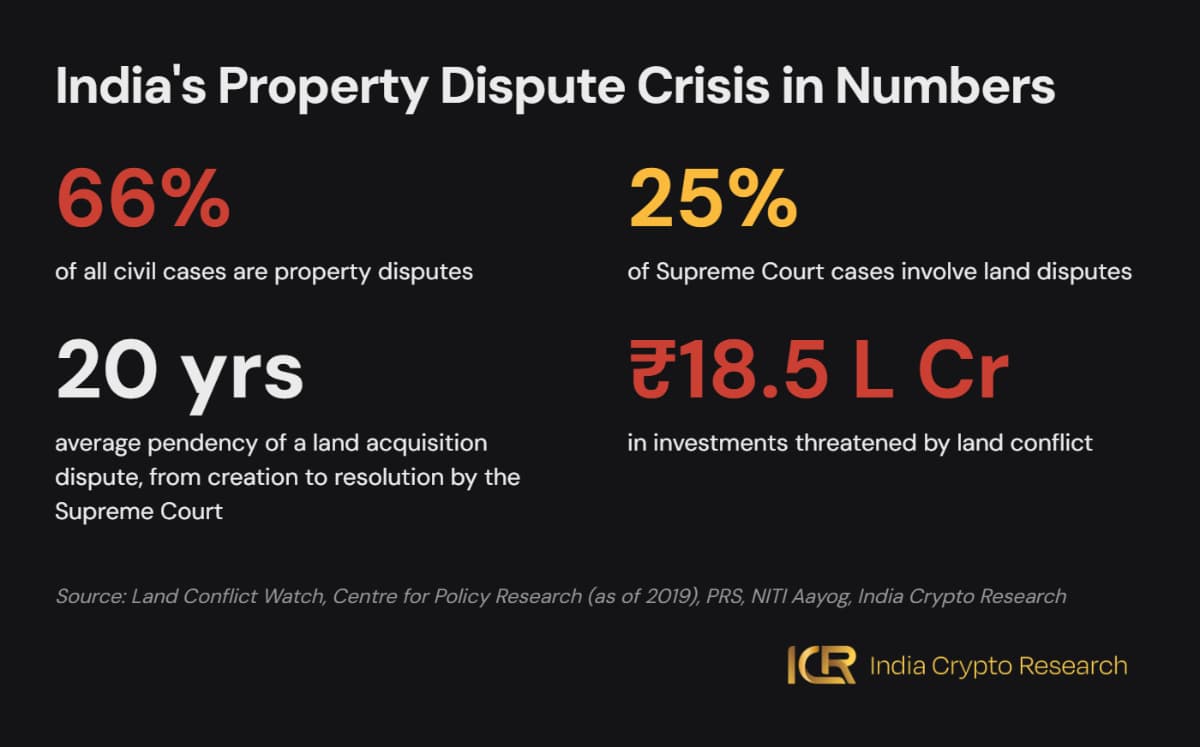

Two Out of Every Three Civil Cases in India Trace Back to a Land Dispute

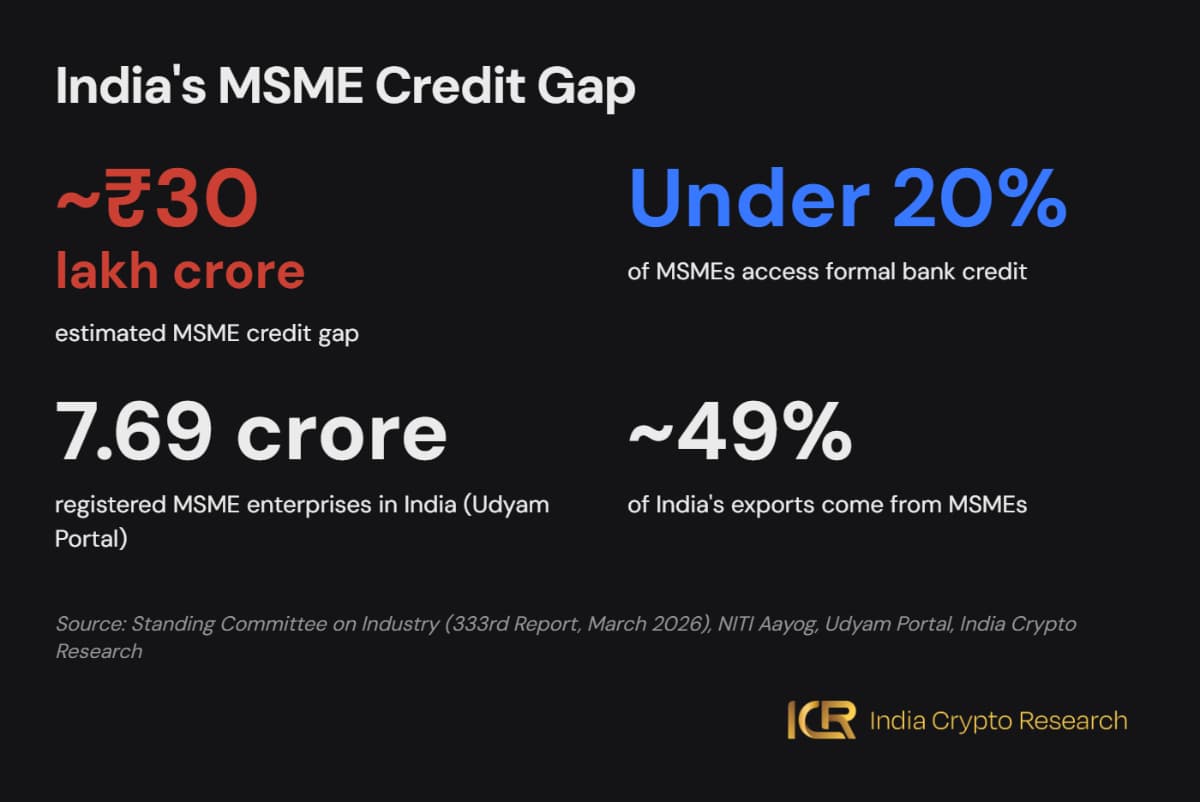

India’s MSME Credit Gap Is ₹30 Lakh Crore, and Disputed Land Records Are Making It Worse

Blockchain Could Be the Fix India's Land Records Problem Has Been Waiting For

Better Land Records Have the Potential to Change How Fast Things Move in India

India Has the Talent and the Use Case, What It Does Not Have Is Regulatory Clarity

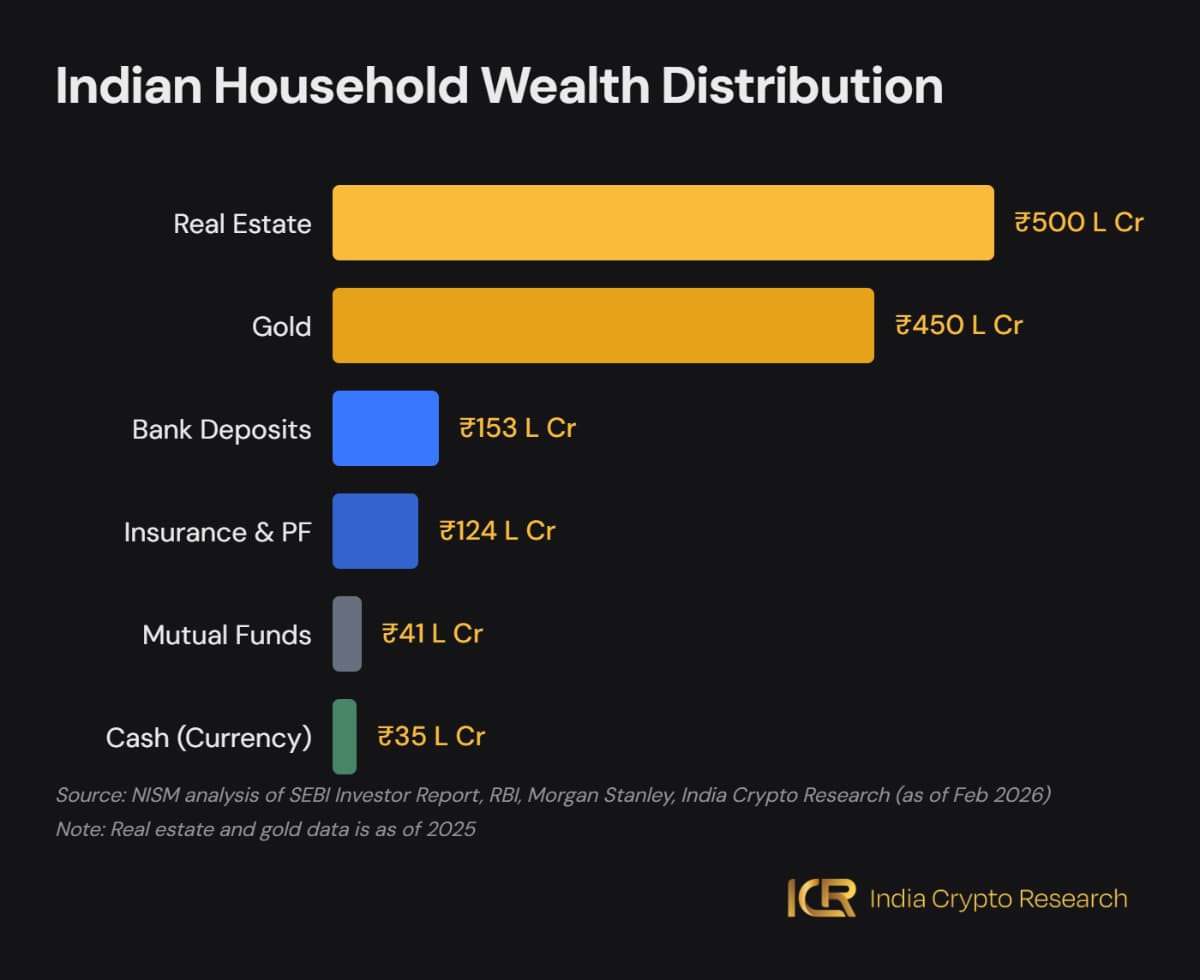

India's households hold roughly ₹500 lakh crore in real estate. That is more than everything they hold in bank deposits, mutual funds, insurance and provident funds combined. Real estate is where most of the country's wealth sits. But for that wealth to work within the financial system, ownership has to be clear and verifiable. In India, ownership disputes over land and property are far more common than most people realise.

Two out of every three civil cases in India are about land or property. At the Supreme Court level, one in four cases is the same story. Around 77 lakh people are currently dealing with active conflicts over 25 lakh hectares of land, with investments worth over ₹18.5 lakh crore sitting in uncertainty, according to the Centre for Policy Research.

And while a dispute drags on, that piece of land cannot be sold, developed, or used to raise any credit. The owner holds the asset on paper. In practice, it is completely out of reach.

The reason goes back to how land record-keeping works in India. Every state has its own registrars and departments, each maintaining different systems that operate in silos. Verifying who owns a piece of land means checking across multiple offices, each holding a different piece of the puzzle. Even after all of that, the picture is often incomplete. And when record-keeping is this scattered, disputes are almost inevitable. What starts as a record-keeping problem quickly becomes an economic one.

India has 7.69 crore registered MSMEs. They employ 32 crore people and contribute roughly 31% of GDP. Yet fewer than 20% of these businesses access formal bank credit today. The credit gap in the sector is estimated at ₹30 lakh crore.

Several factors contribute to this. But collateral sits at the centre of it. Before a bank lends against any asset, it needs to answer two questions: who owns it, and does anyone else have a claim on it? When land records are disputed or scattered across inconsistent registries, answering those questions takes weeks of legal work. For large corporations, this is manageable. For a small business owner with a factory worth ₹50 crore but an unclear title, it often means the loan simply does not happen.

The asset has market value. It does not have financial utility. And that distinction is what keeps crores worth of productive capacity sitting idle, unable to generate the credit that businesses actually need to grow.

At its core, blockchain is a shared digital ledger. When a record is entered, it is time-stamped, tamper-proof, and visible to every authorised party on the network. No single institution controls it. No single institution can alter it. Everyone, the bank, the registrar, the borrower, the court, works off the same version of the truth.

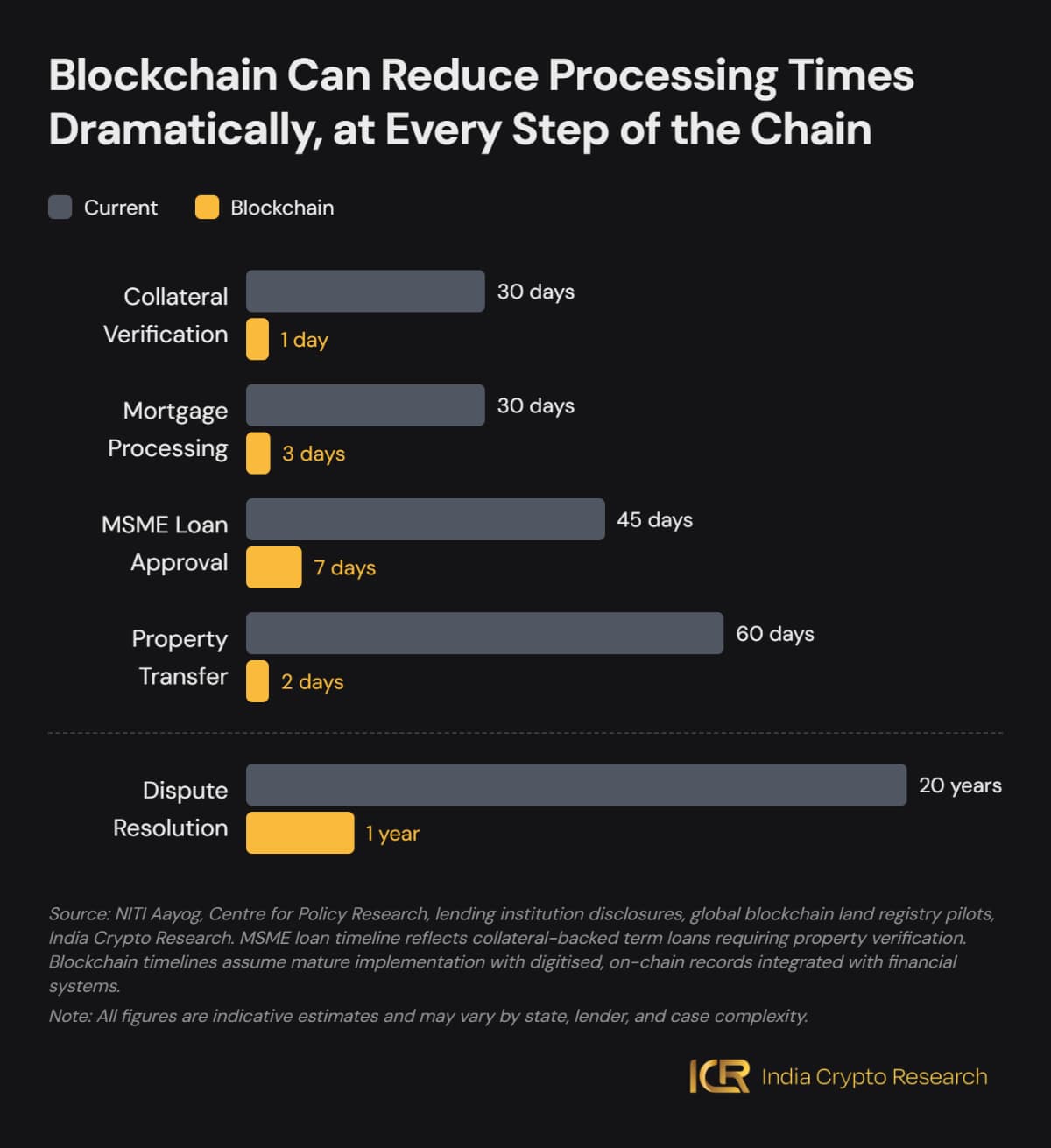

For land records, this changes everything. If a property has an existing dispute or has already been pledged as collateral, it shows up immediately. There is no chasing documents across offices. No weeks of manual cross-referencing. A verification that currently takes weeks becomes a single query.

This is already working in other countries. Georgia registered over 3 lakh land titles on blockchain and is now among the easiest places in the world to register property, as recognised by the World Bank. Sweden has been running similar pilots since 2016. In India, Andhra Pradesh, Telangana and Chhattisgarh have tested blockchain land registries. The Supreme Court has also asked the Law Commission to study how this can be integrated into India's property registration system.

The efficiency gains here are significant:

These are estimates, and actual timelines will vary case by case and across states, but the scale of the difference speaks for itself.

But the bigger shift is structural. With verified, reliable ownership records, MSMEs could pledge fractional portions of an asset rather than putting up an entire property as collateral for a single loan. A business owner who needs ₹10 crore does not have to mortgage a ₹50 crore factory. That kind of flexibility does not exist today because the underlying records cannot support it.

Clean records do not just speed things up. They change what is possible.

India accounts for 12% of global blockchain developers and consistently ranks at the top of global crypto adoption indices. The talent is here. The problem to solve is here. What is missing is a regulatory framework that gives institutions the confidence to act on it.

Digital assets in India still have no clear legal classification. The 2022 tax rules addressed what crypto holders owe the government. They did not answer whether a blockchain land record carries legal finality, or what framework governs a tokenised property used as MSME collateral. Without those answers, every pilot programme hits the same ceiling.

The path forward is not complicated. Standardise existing land records. Build blockchain registries on top. Create a coordinating body to drive implementation across institutions. Each step builds on the previous one. Faster verification leads to faster lending. Better collateral utilisation follows. And ₹30 lakh crore in potential credit that is currently sitting frozen finally has somewhere to go.

Very few have gone beyond the surface to see the broader economic potential it holds. For a country sitting on ₹500 lakh crore in real estate wealth and a ₹30 lakh crore credit gap, that potential is too large to ignore.

India Crypto Research operates independently. The information presented herein is intended solely for educational and informational purposes and should not be construed as financial advice. Before making any financial decisions, it's essential to undertake your own thorough research and analysis. If you're uncertain about any financial matters, we strongly recommend seeking guidance from an impartial financial advisor.