When Borrowing Slows, Fees Follow

Why Price and Fees Do Not Always Move Together

How Aave Compares to the Rest of the Market

What This All Adds Up To

FAQs

Lending is one of the oldest businesses in finance. Someone has capital they are not using, someone else needs it, and the person in the middle earns a spread for making the connection. Banks have done this for centuries, taking deposits from savers and lending them out to borrowers, earning the difference as revenue.

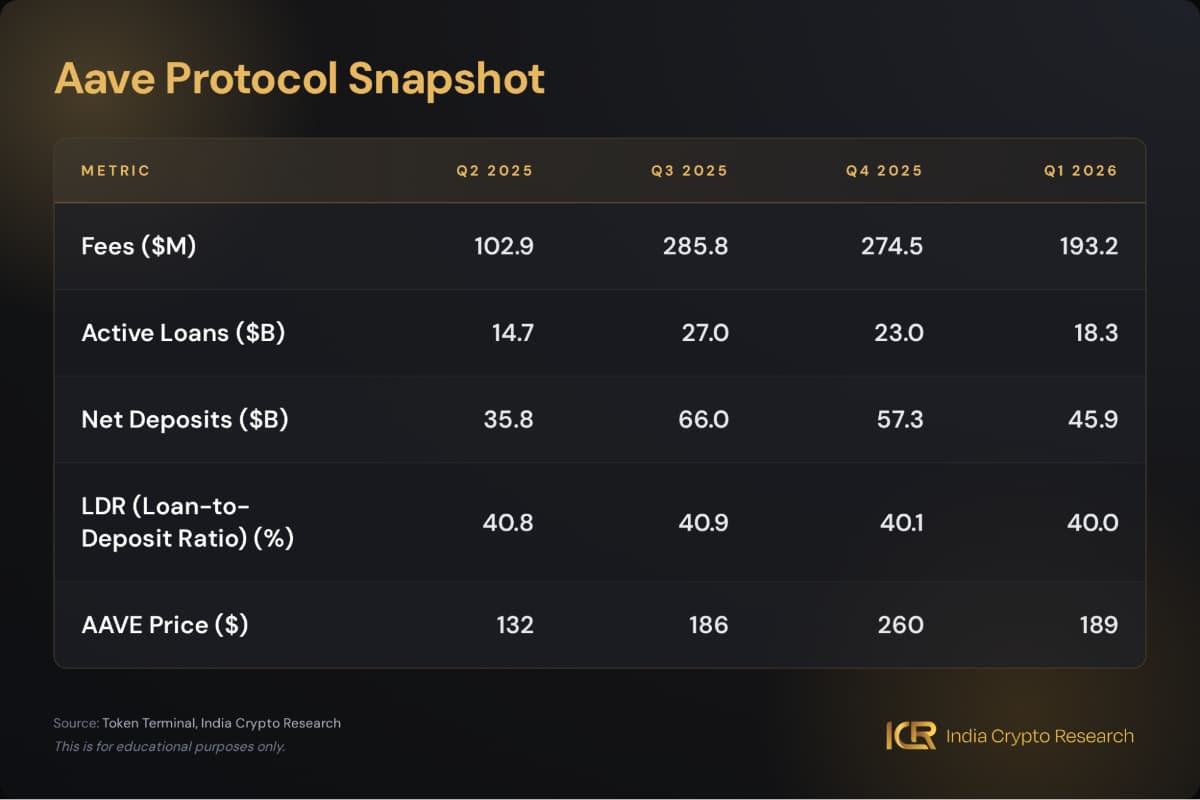

Aave does the same thing, except there is no bank: no branch, no relationship manager, no credit committee. Smart contracts handle the matching automatically, and the interest rates adjust in real time based on how much of the available capital is being borrowed. Over the past year, Aave processed $856 million in fees doing exactly this. Here is what the numbers show about where it stands today.

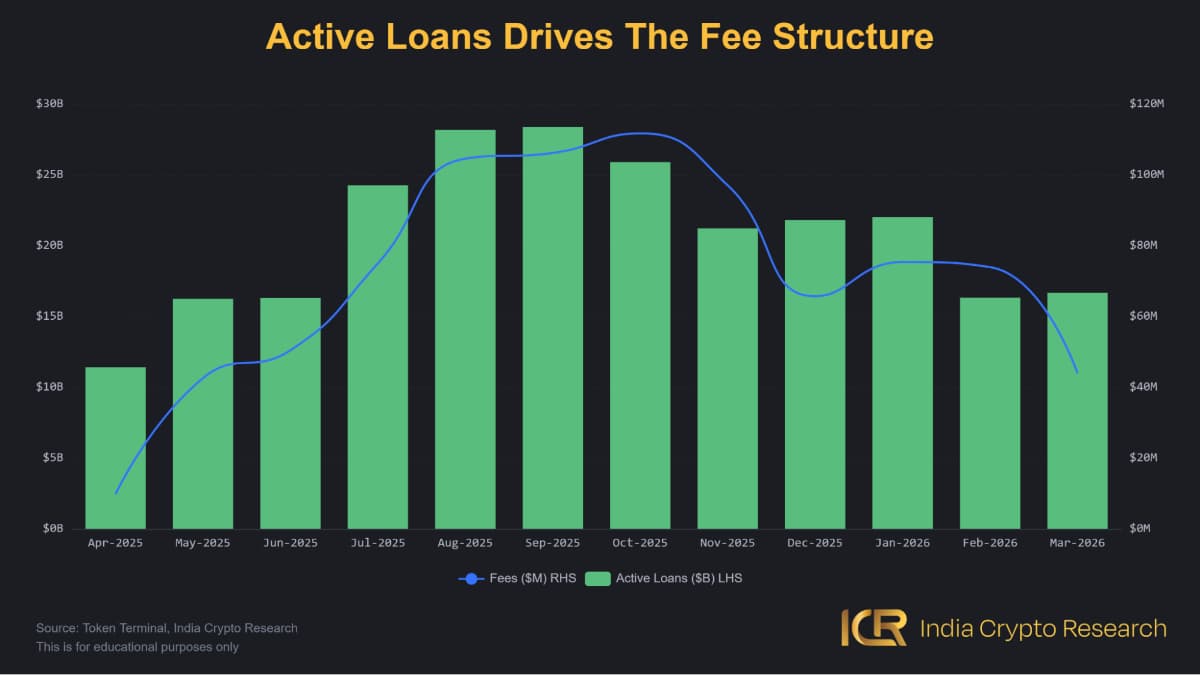

Aave earns fees three ways: borrow interest, flash loan fees, and liquidation fees. Borrow interest dominates by a wide margin. And the borrowing interest is simply the interest rate multiplied by the total volume of outstanding loans. Which means fees and active loans move together, almost mechanically.

Active loans peaked at an average of $27B in Q3 2025. By Q1 2026, that had fallen to $18.3B, a 32% drop. Fees fell from $285.8M to $193.2M over the same period. The fee drop was proportionally steeper because interest rates across DeFi also declined as borrowing demand softened. Less demand meant lower rates, which meant lower fees even on the loans that remained.

What drove the surge in the first place? Net deposits grew from $35.8B in Q2 2025 to $66B in Q3, an 84% expansion in a single quarter. More capital meant more borrowing capacity. Borrowers showed up. Fees followed. The contraction since is the same dynamic in reverse.

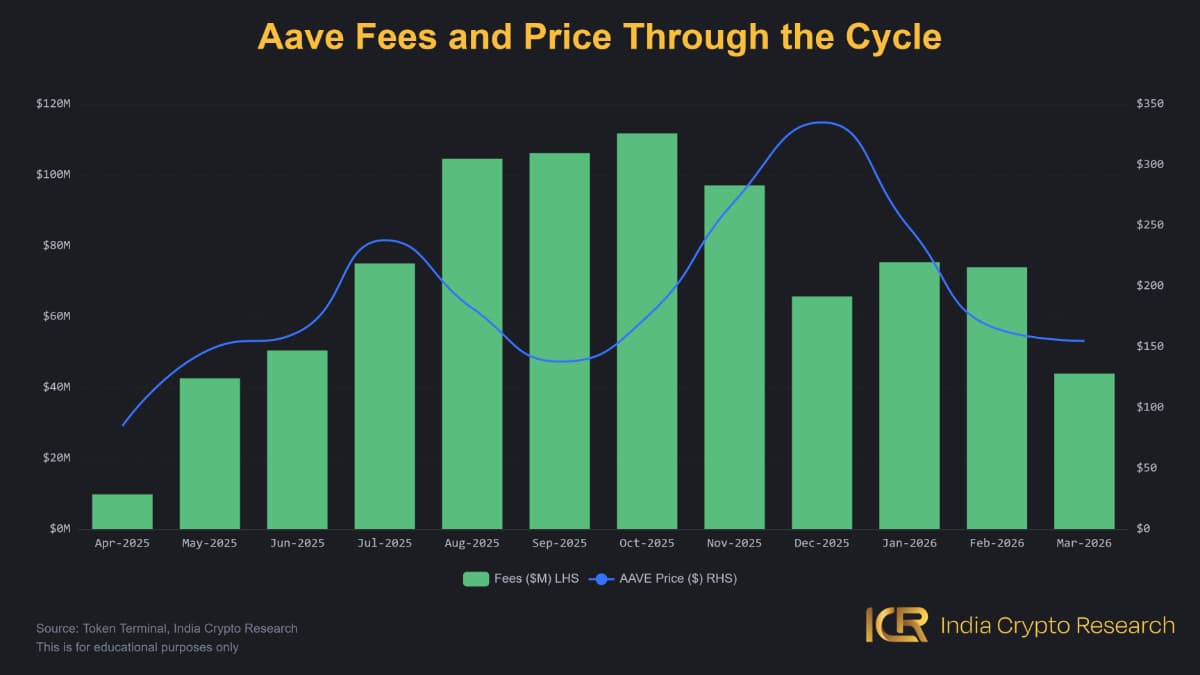

Q4 2025 is the most instructive quarter in this dataset.

Fees were $274.5M, nearly identical to Q3's $285.8M. Basically flat. But the average AAVE price jumped from $186 to $260, and in December alone it hit $335. The fee trajectory had not changed. The broader crypto market peaked in late 2025 and lifted almost every token with it, regardless of protocol performance. Think of it like a rising tide. Sentiment, not fundamentals, drove AAVE to $335.

Then Q1 2026 arrived. Fees fell to $193.2M. The average price corrected to $189. The market had caught up to where fundamentals actually were.

The cleaner relationship is Q2 to Q3 2025: fees nearly tripled, price went from $132 to $186. When the protocol's own metrics are driving the move, price and fees track each other. When macro sentiment takes over, the price disconnects temporarily and then corrects back.

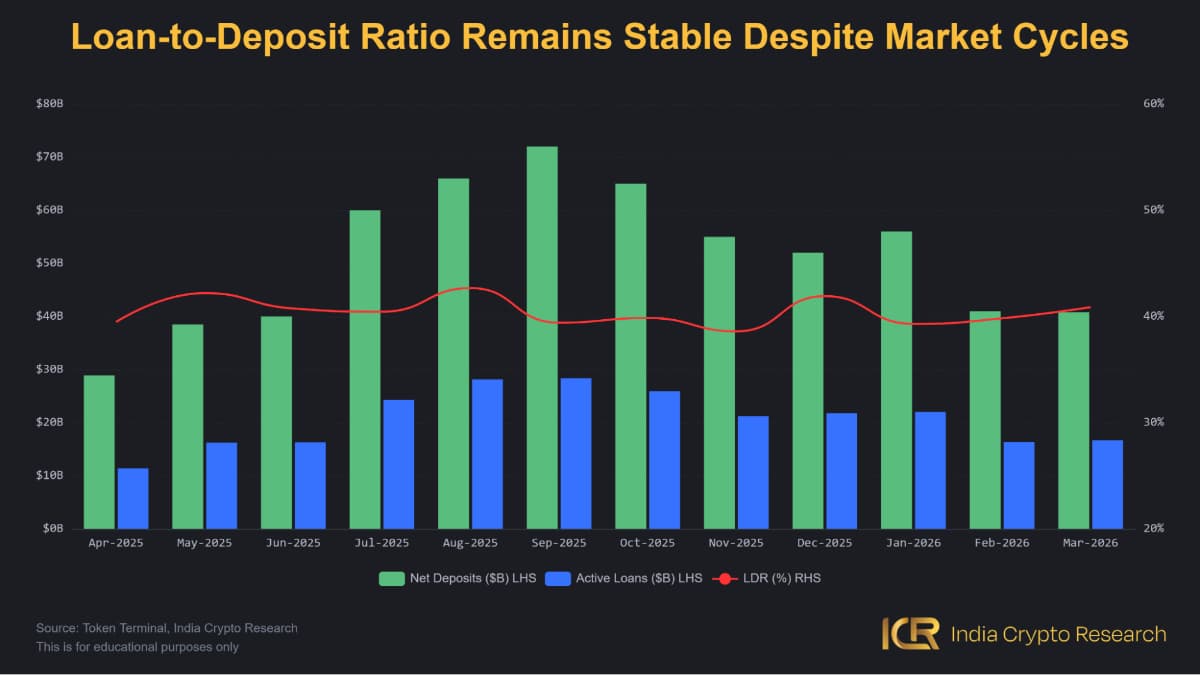

The loan-to-deposit ratio held at 40% through every quarter, which tells you both deposits and loans contracted proportionally. But understanding whether Aave is actually healthy requires looking at how it performed relative to competitors over the same period.

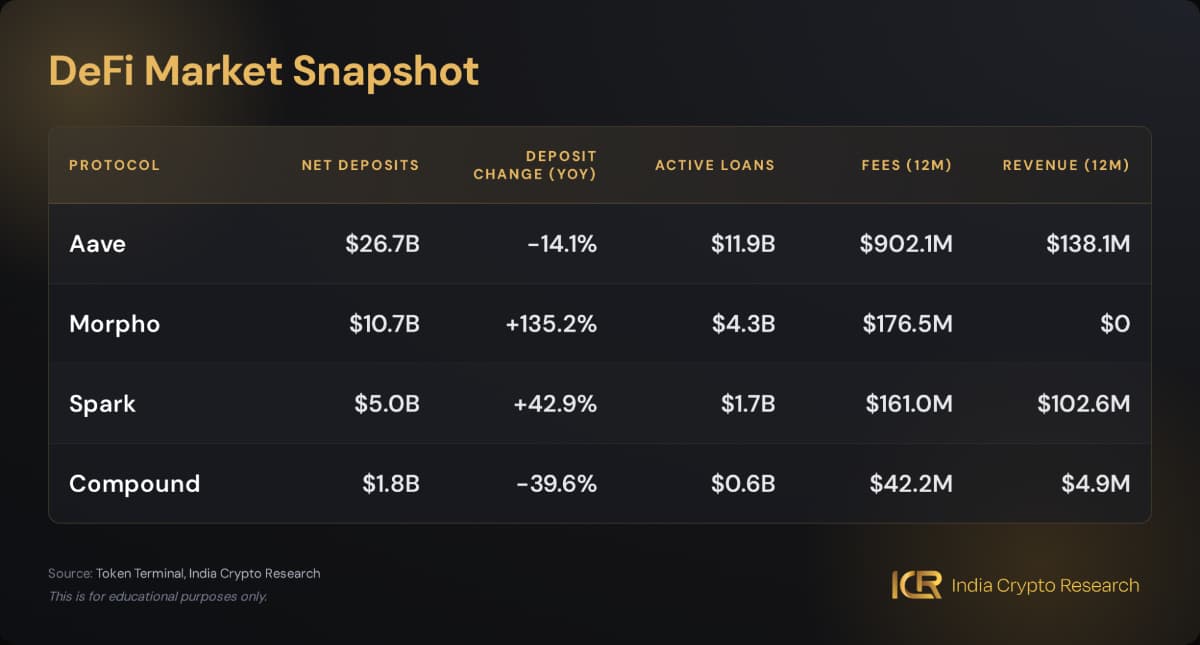

Here is how the four major DeFi lending protocols stack up today, based on trailing 12-month data.

A few things stand out.

Morpho has grown its deposits by 135.2% in a year and now holds 24.2% of the market. That growth is real, and it is happening while Aave's deposits fell 14.1%. Aave is losing deposit share. The data is clear on that.

But context matters. Aave still holds 60.4% of total deposits and 64.6% of active loans across these four protocols. And despite the deposit decline, Aave's active loans are actually up 4.7% year over year. Deposits fell, but borrowers stayed. The platform lost supply-side capital faster than it lost demand-side activity.

The more important comparison is on revenue. Morpho has generated $176.5M in fees over the past 12 months and zero in protocol revenue. That is not an accounting quirk. Morpho has not yet turned on a protocol fee switch, meaning all fees flow to depositors and liquidity providers rather than to the protocol itself. Morpho is buying market share by passing all economics to users. That is a viable growth strategy, but it means Morpho is not yet a self-sustaining business in the way Aave is.

Aave earned $138.1M in protocol revenue over the same period. Compound earned $4.9M and is clearly losing ground, with deposits down 39.6% and fees trending down 34.2%.

The full picture is more nuanced than either the bear or bull case suggests.

On the negative side: Aave's deposits are down 14.1% year over year. Morpho is growing fast and taking market share. Fee compression from Q3 2025 to Q1 2026 is real. These are not things to dismiss.

On the positive side: Aave still dominates by a wide margin. Its active loans are up year over year, even as deposits fell, which means the borrower base held up. It earned $138.1M in actual protocol revenue over 12 months, far more than Morpho, which is currently earning nothing at the protocol level. And the fee decline is directly explained by lower active loan volumes, not by anything structurally breaking inside the protocol.

The question heading into the rest of 2026 is whether Morpho eventually turns on its protocol fee switch, which would make the competitive picture sharper, and whether Aave's deposit base stabilises or continues to lose ground. Those two variables will shape the DeFi market share story more than anything else.l

For now, Aave's fee engine is intact. The borrower base held through the correction. The protocol is generating real revenue. And the competition, while real, has not yet demonstrated that it can sustain its growth model without subsidising users through zero protocol fees.

Note : Not an Investment Advice ,This is for educational purposes only.

India Crypto Research operates independently. The information presented herein is intended solely for educational and informational purposes and should not be construed as financial advice. Before making any financial decisions, it's essential to undertake your own thorough research and analysis. If you're uncertain about any financial matters, we strongly recommend seeking guidance from an impartial financial advisor.