Understanding the MPID Act

Why was the amendment necessary?

Amendment 1: Virtual Digital Assets become part of "deposits"

Amendment 2: Faster proceedings through limited adjournments

Amendment 3: A 50% pre-deposit requirement before appeal

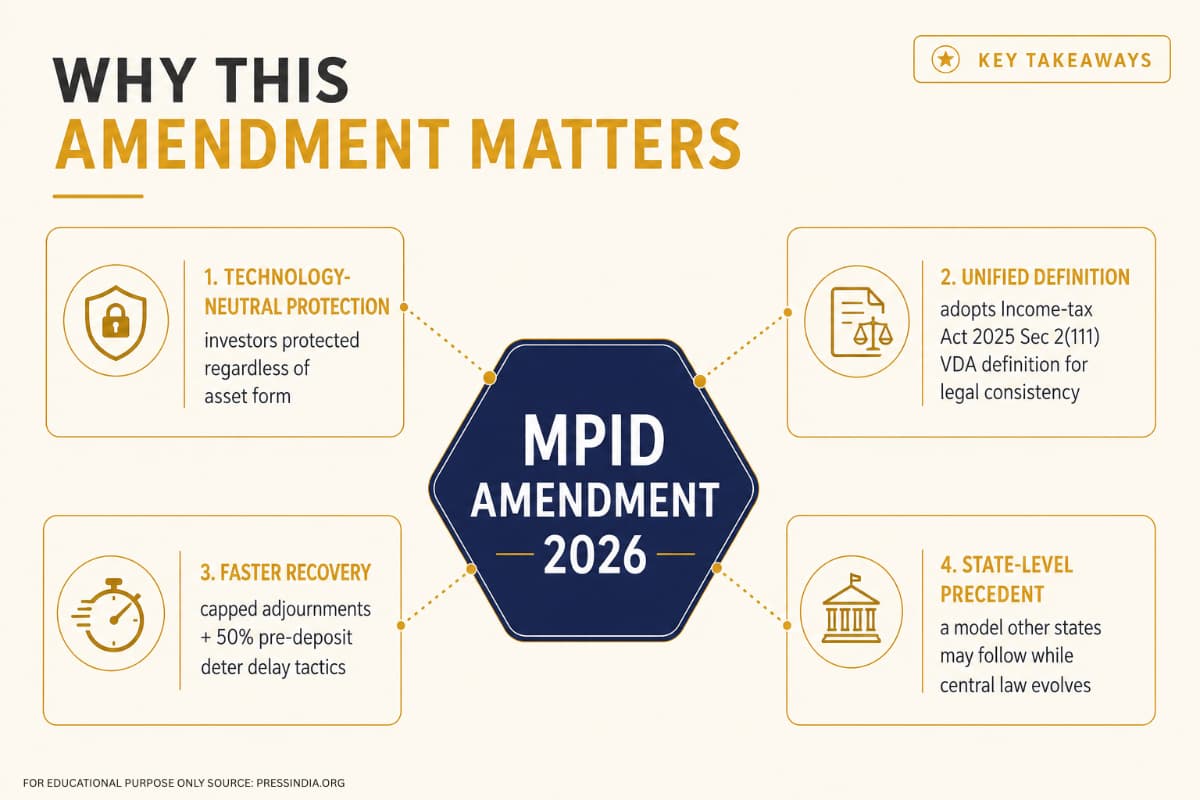

Why does this amendment matter?

Why Maharashtra?

Looking ahead

How Maharashtra's latest amendment brings Virtual Digital Assets under investor protection and what it signals for India's evolving crypto regulatory landscape.

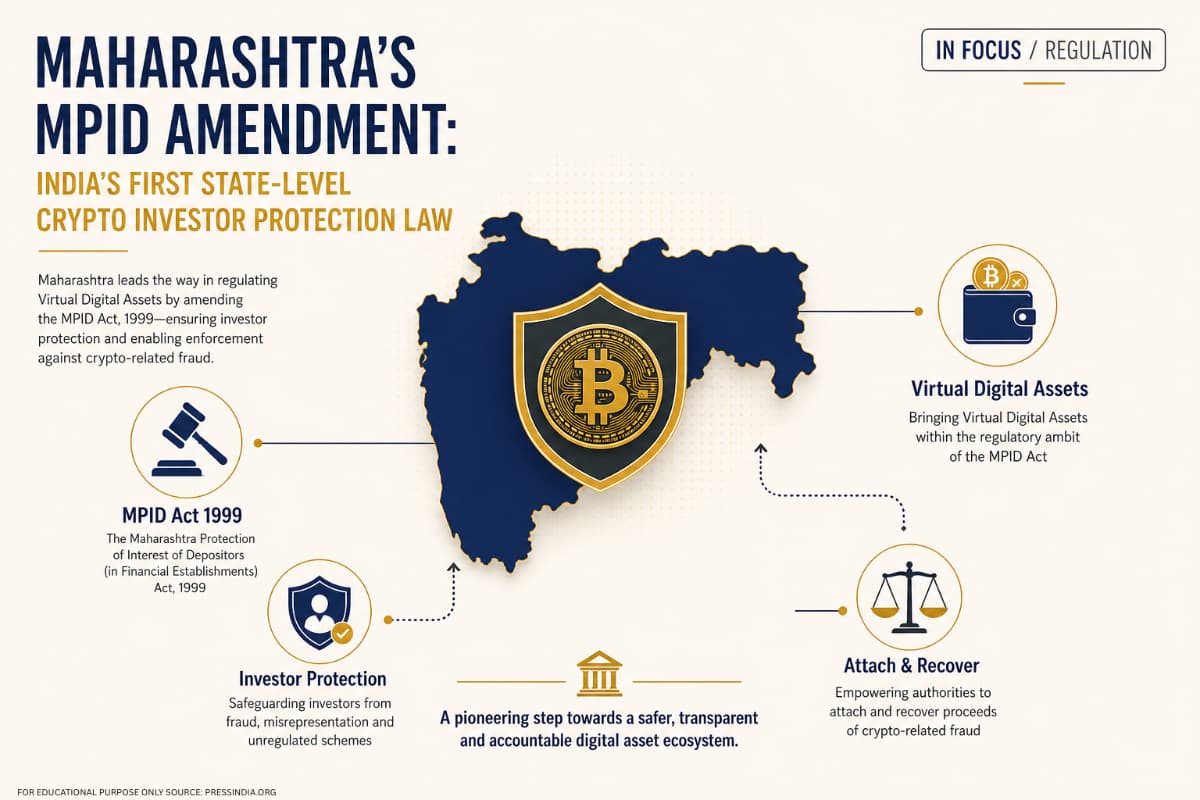

For years, India's cryptocurrency debate has rallied around taxation, anti-money laundering compliance, exchange regulation, and the debate has centered on whether digital assets should be recognized as legal financial instruments. While the Union Government continues to debate on a comprehensive regulatory framework, Maharashtra has quietly taken a pivotal step not by regulating cryptocurrency itself, but by enhancing investor protection in an era where financial fraud is more and more digital.

On 30 June 2026, the Maharashtra Government launched the Maharashtra Protection of Interest of Depositors (in Financial Establishments) (Amendment) Bill, 2026. At first glance, the amendment appears procedural, comprising of only a few pages. However, its impact extend well beyond procedural reform. For the first time, a state has specifically placed Virtual Digital Assets (VDAs) under the purview of an existing depositor protection law, recognizing that financial fraud has shifted from cash-based schemes to blockchain-enabled investment scams.

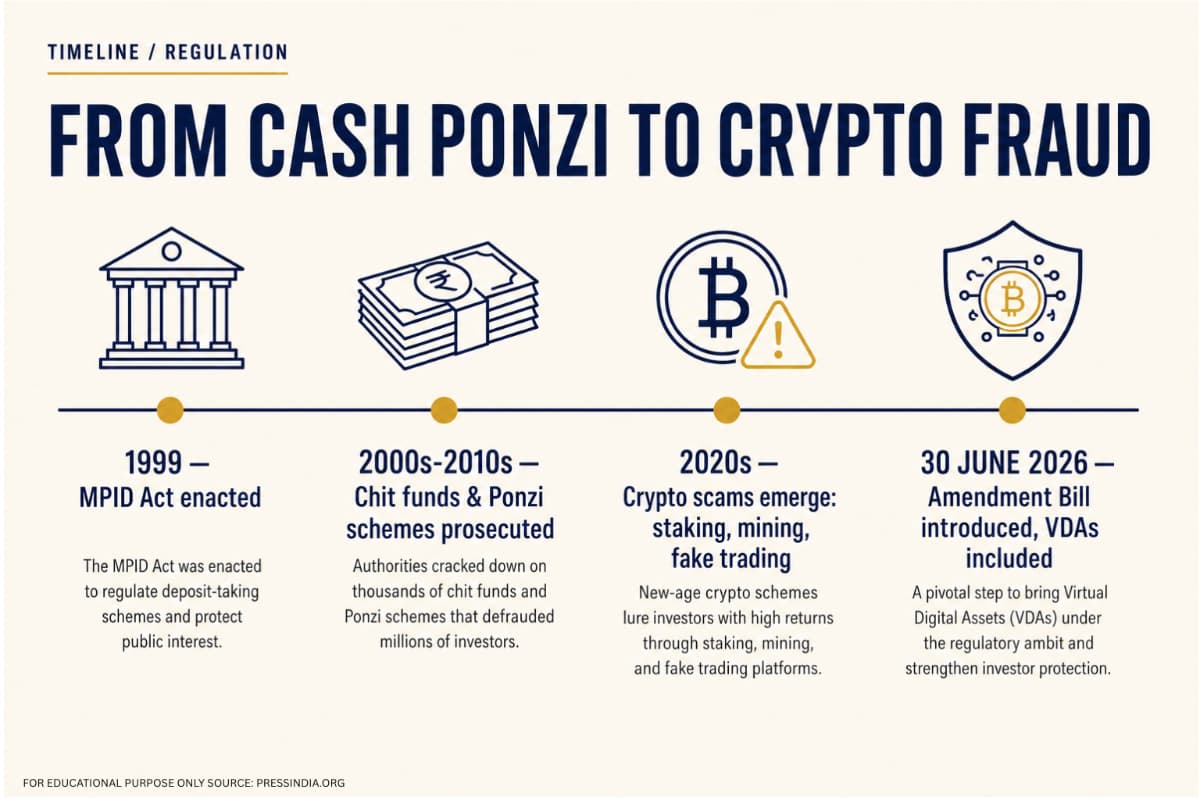

The Maharashtra Protection of Interest of Depositors (MPID) Act was passed in 1999 to protect investors from illegitimate financial establishments that collect deposits and thereafter default on repayment. The legislation enables the state to attach the properties of defaulter entities, establish designated courts, and facilitate the recovery of funds for affected depositors.

In the past, the Act has been used against Ponzi schemes, unregulated deposit-taking entities, chit fund operators, and fraudulent finance companies. Yet, when the legislation was formulated in 1999, cryptocurrencies and blockchain-based digital assets was not existent in the financial ecosystem. Consequently, the law was never designed to address investment schemes where deposits are collected in Bitcoin, stablecoins, or other digital assets.

This gap has become increasingly pivotal as fraudsters adopt cryptocurrencies as a preferred medium for soliciting investments.

The Government's own Statement of Objects and Reasons offers an explicit rationale. It observes that financial frauds, unauthorized deposit schemes, and investor deception are increasingly being carried out through cryptocurrencies, digital coins, and other blockchain-based digital instruments. Simultaneously, the existing definition of "deposit" under the MPID Act did not precisely include Virtual Digital Assets. Thus, the Government considered it necessary to amend the legislation and bring these assets within its legal infrastructure.

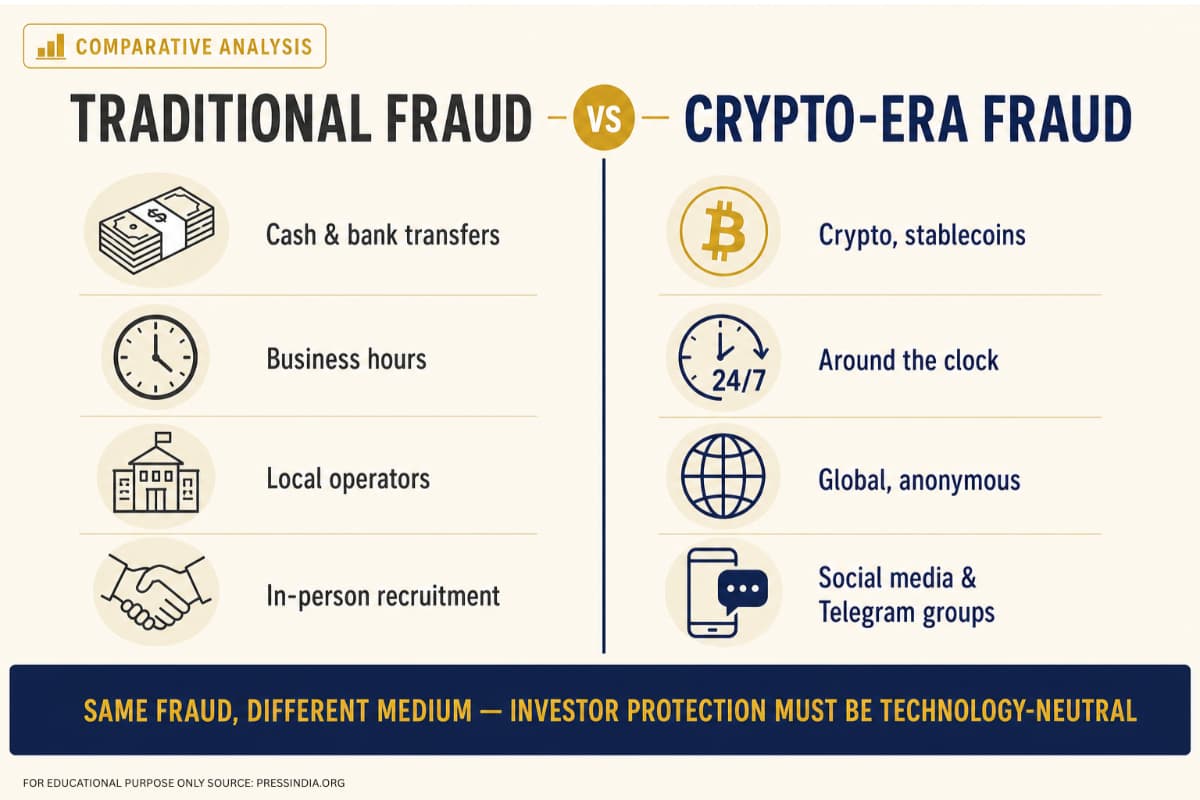

This reflects an important policy realignment. Instead of classifying cryptocurrency solely as a speculative asset or tax consideration, the amendment acknowledges that digital assets can simultaneously serves as vehicles for financial fraud. The focus, therefore, is not on regulating cryptocurrency markets but on ensuring that investors remain defended regardless of whether fraud occurs through cash, gold, or blockchain-based assets.

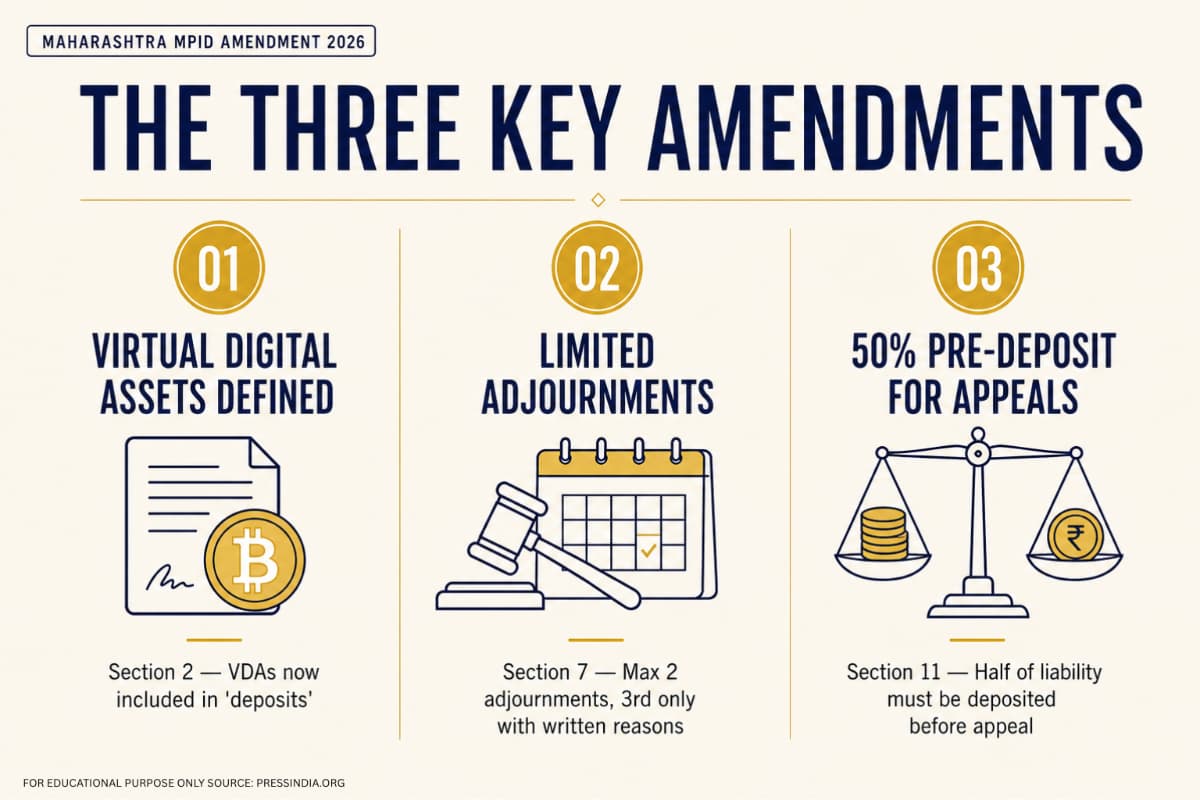

The most pivotal amendment is found in Section 2 of the Act. The definition of "deposit" has been expanded by introducing the words "or any Virtual Digital Asset" after "valuable commodity." Moreover, the amendment introduces a formal definition of "Virtual Digital Asset" by adopting the meaning assigned under Section 2(111) of the Income-tax Act, 2025.

Although seemingly compact, this amendment has substantial legal magnitude.

Before, if a fraudulent financial establishment collected Bitcoin, Ether, or stablecoins from investors, questions could emerge regarding whether such digital assets fell within the purview of the MPID Act. By precisely incorporating Virtual Digital Assets into the definition of deposits, the amendment removes this obscurity. It enables enforcement authorities to pursue recovery proceedings involving crypto-based investment schemes under the same legal infrastructure that has historically been applied to traditional financial frauds.

Equally noteworthy is the decision to rely on the Income-tax Act's definition of Virtual Digital Assets rather than creating a separate legal framework definition. This promotes consistency across legal frameworks and reduces the risk of conflicting interpretations between taxation and investor protection laws.

The amendment also seeks to improve procedural efficiency. It inserts a new provision under Section 7 restricting the number of adjournments that may be granted in proceedings before the Designated Court.

Under the amended framework, courts may grant a maximum of two adjournments. A third adjournment is permitted only in exceptional circumstances and only after the court records written reasons explaining why such an extension is compulsory in the interest of justice.

According to the Government, this change is designed to expedite proceedings and aligns the MPID Act with the wider procedural reforms introduced under the Bharatiya Nagarik Suraksha Sanhita, 2023.

For investors, this amendment is specifically relevant. Recovery proceedings in financial fraud cases often extend over several years, reducing the likelihood of timely compensation. By limiting repeated adjournments, the Government drives to enhance the efficiency of designated courts and accelerate the recovery process.

The amendment introduces a clause under Section 11 requiring a financial entity to deposit 50% of its aggregate liability with the Competent Authority before its appeal against a Designated Court's order can be entertained.

The Government explains that appeals were, in some cases, being used primarily as a tactic to delay the recovery of deposits rather than to challenge judicial decisions on valid legal grounds. The pre-deposit requirement seeks to discourage such practices while safe guarding the right to appeal.

This provision also aligns with a wide-ranging legislative trend in India, where pre-deposit requirements exist in several tax and regulatory statutes to prevent baseless litigation while ensuring that legitimate appeals remain available.

The importance of this amendment extends beyond Maharashtra.

It signifies one of the clearest acknowledgements by an Indian state that financial fraud has evolved alongside technological innovation. Investment scams no longer rely solely on cash or bank transfers. Fraudsters increasingly solicit investments in cryptocurrencies, stablecoins, and other blockchain-based assets, making it vital for investor protection laws to evolve accordingly.

Significantly, the amendment should not be interpreted as crypto regulation. It neither legalizes nor bans cryptocurrency trading, nor does it establish licensing requirements for digital asset establishments. Instead, it strengthens the state's ability to protect investors when cryptocurrencies are used as instruments of fraud.

The legislation itself does not explain why Maharashtra introduced this amendment before other states. However, Maharashtra has long operated one of India's most active depositor protection frameworks under the MPID Act and has substantial institutional experience dealing with intricate financial fraud through designated courts and enforcement agencies. The amendment therefore appears to be a logical reformation of an existing legal framework rather than the inception of an entirely new regulatory regime.

Whether other states adopt similar amendments remains to be seen. If they do, Maharashtra's approach may well serve as a legislative template for integrating digital assets into existing investor protection laws across India.

India's crypto policy has often been discussed from the perspective of taxation, anti-money laundering compliance, and the absence of comprehensive national legislation. The MPID Amendment introduces another angle to this conversation: investor protection.

Rather than waiting for a comprehensive national crypto law, Maharashtra has proved that existing legal frameworks can be amended to address emerging forms of financial malpractice. It is a targeted reform that acknowledges how technology has transformed the methods through which financial fraud is executed, while reaffirming that investor protection should remain technology-neutral.

As digital assets become increasingly integrated into financial markets, this amendment may prove to be a landmark precedent not because it regulates cryptocurrency, but because it ensures that the law continues to protect investors irrespective of the form in which fraudulent deposits are collected.

FOR EDUCATIONAL PURPOSES ONLY. SOURCE: PRESSINDIA.ORG

India Crypto Research operates independently. The information presented herein is intended solely for educational and informational purposes and should not be construed as financial advice. Before making any financial decisions, it's essential to undertake your own thorough research and analysis. If you're uncertain about any financial matters, we strongly recommend seeking guidance from an impartial financial advisor.