How the tax department gets this information

Where crypto tax filing gets complicated

What an inaccurate return costs now

What this means for filing this year

File it with India Crypto Research

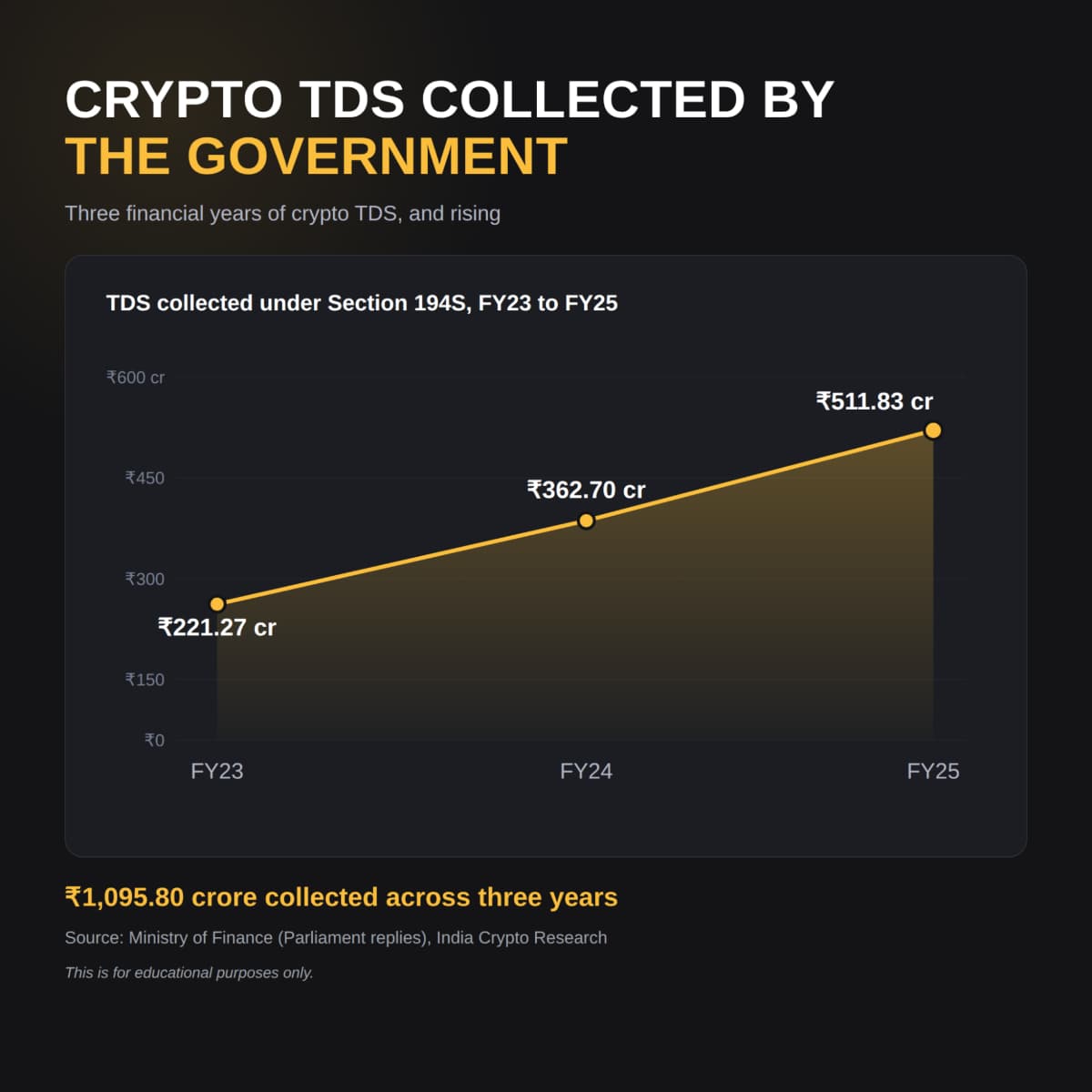

The government collected ₹511.83 crore in crypto TDS in FY25, its biggest year yet. That number is the visible part. The part most traders miss is that the Income Tax Department no longer has to guess who traded. The exchanges already report it directly, which means your crypto activity is on file before you sit down to declare it.

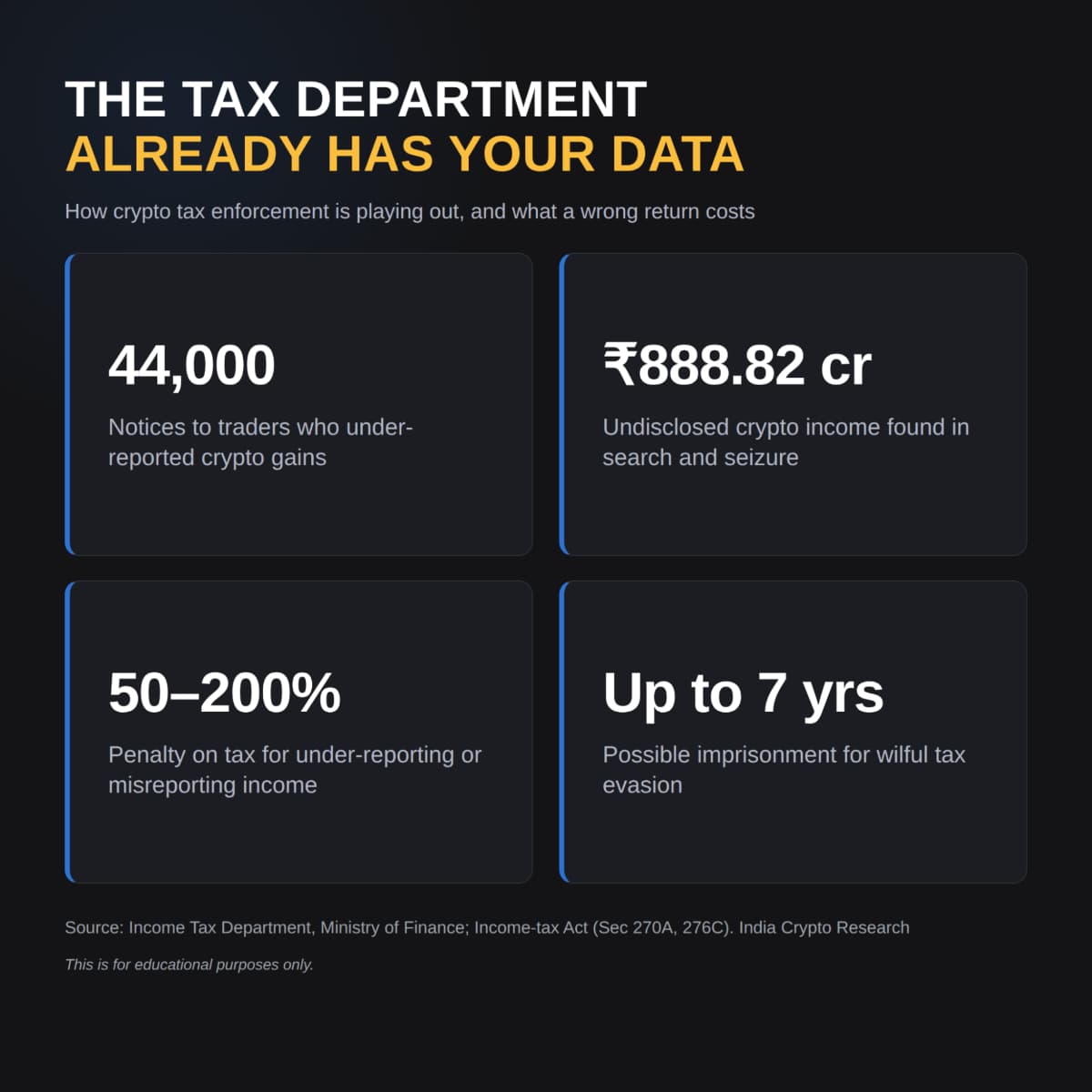

Crypto exchanges already report TDS and transaction data to the Income Tax Department, and that reporting is what drives enforcement. Using analytics tools to match exchange data against filed returns, the department has issued over 44,000 notices to traders who under-reported crypto gains, and has uncovered ₹888.82 crore of undisclosed income through search and seizure operations. The collection numbers point the same way. TDS from crypto has gone up every year, from ₹221.27 crore in FY23 to ₹362.70 crore in FY24 to ₹511.83 crore in FY25, taking the three-year total to ₹1,095.80 crore. Each of those rupees is tied to a specific transaction the department can trace. From April 2026, a dedicated reporting framework under the Income Tax Act 2025 tighten this further, requiring exchanges to file standardised statements of crypto transactions. So a crypto trade is no longer something that stays between you and your exchange.

Most people know the headline rule. Gains on virtual digital assets are taxed at a flat 30% under Section 115BBH, with nothing deductible beyond the cost of acquisition. The complications sit below that. A loss on one coin cannot be set off against a gain on another, and losses cannot be carried forward, so each position is taxed on its own. The 1% TDS under Section 194S is charged on the sale value of every transfer rather than on profit, so over a year of trading, it adds up to a long list of small credits, each of which has to be matched back against your final tax. For anyone who trades regularly, Schedule VDA is not a single figure you enter. It is a transaction-by-transaction record of every buy, sell, cost and TDS deduction, and that reconciliation is where most filing mistakes happen.

The cost of getting this wrong sits in the existing penalty rules, and they are not light. Under-reporting income attracts a penalty of 50% of the tax due, and misreporting attracts 200%, on top of interest at 1% a month and, in cases of wilful evasion, prosecution that can carry imprisonment of up to seven years. Because the exchange data reaches the department on its own, a gap between your return and its records usually surfaces through a routine data match rather than a manual check. The new framework adds pressure from the other side, too: from April 2026, exchanges themselves face penalties for failing to report crypto transactions accurately, which means the data your return gets checked against is only going to get cleaner.

None of this makes crypto taxation in India heavier than it was. The rates and the core rules for taxpayers are the same as last year. What is different is that the room to get it wrong, whether by mistake or otherwise, has narrowed. The department is no longer working from what taxpayers choose to report. It is working from the actual transaction data, and your return now gets checked against it. For anyone who traded crypto, that makes an accurate, well-reconciled filing worth getting right, this year and for every past year still open to assessment.

India Crypto Research's Crypto Tax calculator works out your exact 30% liability, applies each 1% TDS credit, and prepares a transaction-level Schedule VDA that lines up with the department's records. If your trading is spread across several exchanges, India Crypto Research can also handle the filing itself, so the reconciliation that catches most people out is taken care of properly.

India Crypto Research operates independently. The information presented herein is intended solely for educational and informational purposes and should not be construed as financial advice. Before making any financial decisions, it's essential to undertake your own thorough research and analysis. If you're uncertain about any financial matters, we strongly recommend seeking guidance from an impartial financial advisor.