What Is Crypto, in Simple Words

How the Indian Government Recognises Crypto

What Are Crypto Taxes in India

Do These Crypto Tax Rules Apply to You

How the ICR Crypto Tax Calculator Works

Crypto in India has moved from curiosity to accountability.

Have you heard of

Most people have. Some have bought it. Some have ignored it. Many have strong opinions about it. But very few people pause to ask what it actually represents.

At its core, crypto is a way to own and move value digitally.

Think about how money works today. Your bank balance is not physical cash. It is a number stored in a system that banks maintain and trust each other to update correctly. Crypto removes the bank from that process and replaces it with technology.

Instead of one institution keeping records, crypto uses a shared digital record that many computers maintain together. When value moves from one person to another, that movement is recorded openly and permanently. This shared record is called a blockchain.

Ownership in crypto works differently as well. You do not rely on a bank account or an institution to confirm what you own. Ownership is proven through a private key, which is a secret code known only to you. If you control the key, you control the crypto. There is no central authority that can reverse this or recover it for you.

To manage these keys, people use wallets. A wallet does not store coins. It stores the credentials that prove ownership and allows value to move securely.

In simple terms:

After hearing about Bitcoin and understanding how crypto works, the next question naturally follows.

If crypto exists outside banks and traditional systems, how does the Indian government look at it?

For a long time, this question created confusion. Some people believed crypto was banned. Others believed it was fully legal. Both views missed an important middle ground.

The Indian government does not treat crypto as money. You cannot replace the Indian rupee with crypto for official payments or obligations. At the same time, the government does not ignore crypto either.

Instead, crypto is recognised as an asset.

Under Indian law, crypto is classified as a Virtual Digital Asset. This classification matters because it answers one key question. If an asset exists, holds value, and is transferred between people, it becomes part of the tax system.

This recognition is practical, not philosophical.

The government is not making a statement about whether crypto is good or bad. It is acknowledging that people are using it, trading it, earning from it, and holding value in it. Once that happens, the activity needs to be visible and accounted for.

This is why taxation entered the picture before broader regulation.

By defining crypto as a Virtual Digital Asset, the government created a framework to track and report activity, even while discussions around investor protection, regulation, and use cases continue.

In simple terms:

This distinction is important. Many people assume taxation means approval, or that regulation means encouragement. In reality, taxation is about accountability. It ensures that economic activity, regardless of form, is reported transparently.

Once crypto was recognised this way, the next step became inevitable. If value is being transferred, the rules of taxation apply.

Now that we understand why crypto is taxed, the next step is understanding how India has structured crypto taxation.

In India, crypto is not taxed by extending rules meant for shares or mutual funds. Instead, a separate regulatory framework was introduced specifically for crypto assets. These assets are classified as Virtual Digital Assets under Indian tax law [1], bringing them under a clearly defined set of rules.

In India, crypto is legally classified as a Virtual Digital Asset (VDA) [2].

A VDA includes:

Once an asset is classified as a VDA, any income arising from its transfer becomes taxable under specific provisions of Indian tax law. This classification is important because it formally brings crypto activity into the tax system, even though crypto is not recognised as legal tender.

In simple terms, VDA status means:

The Indian crypto tax framework is built around three regulatory pillars.

Any income arising from the transfer of crypto is taxed at a flat rate of 30%. This rate applies regardless of how long the crypto was held. Indian regulations do not recognise short-term or long-term holding periods for crypto.

For example, if crypto bought for ₹1,00,000 is sold for ₹1,50,000, the profit of ₹50,000 is taxed at 30 %, resulting in a tax liability of ₹15,000.

Indian crypto tax rules allow extremely limited deductions. In most cases, only the cost of acquisition is permitted to be deducted from the selling value.

Expenses such as:

are generally not allowed as deductions.

Using the earlier example:

No other costs can be used to reduce this amount.

To ensure visibility of crypto activity, Indian tax regulations introduced 1% Tax Deducted at Source (TDS) on crypto transactions under Section 194S [3].

TDS applies only after certain annual transaction value limits are crossed:

Once the applicable threshold is breached, 1% TDS is deducted on the value of each eligible crypto transaction.

TDS is deducted at the time a crypto transfer takes place and is calculated on the gross transaction value, not on profit.

For example:

TDS does not replace income tax. It functions as a reporting and tracking mechanism, ensuring that crypto transactions remain visible within the tax system.

Together, the flat tax on profits, limited deductions, and transaction-level TDS form the foundation of crypto taxation in India. While the framework may feel strict compared to other asset classes, it reflects a regulatory focus on traceability and disclosure.

At this stage, one point is worth emphasising. Crypto taxation in India is not only about how much tax you pay. It is equally about how clearly your crypto activity is recorded, reported, and reconciled under the law.

After understanding how crypto is taxed, the next question becomes personal.

Does this apply to you?

In India, crypto taxation is not based on labels such as trader, investor, or beginner. It is based on activity. If you engage with crypto in a way that creates or transfers value, the tax framework applies.

This means taxation is linked to what you do, not what you intend.

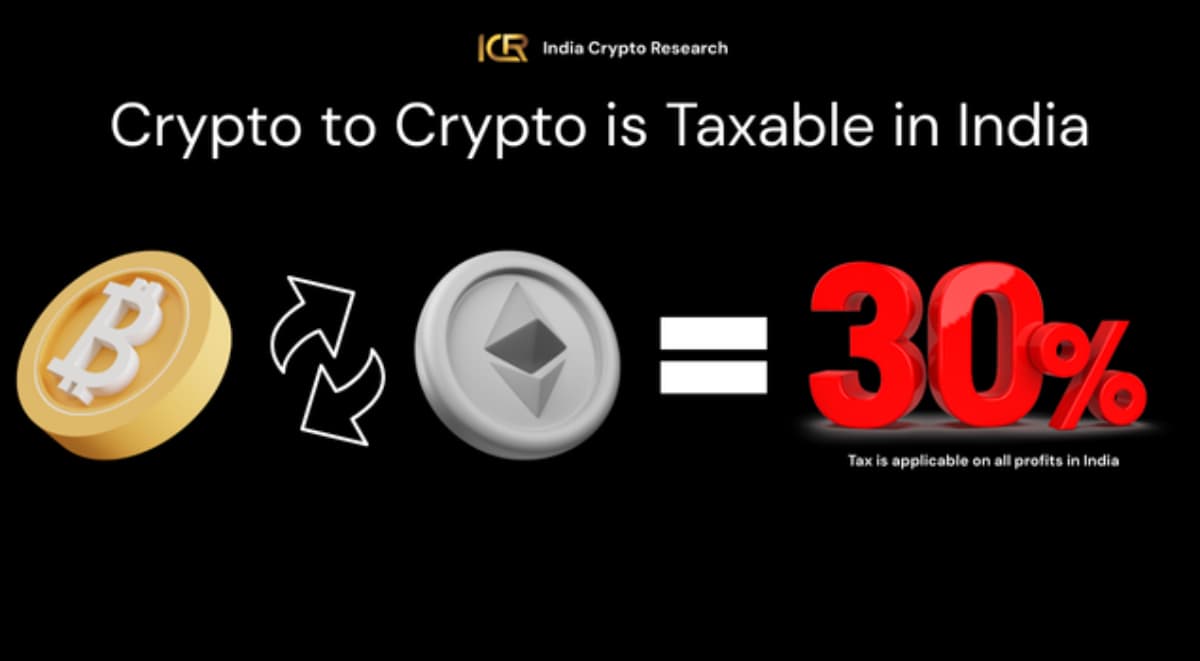

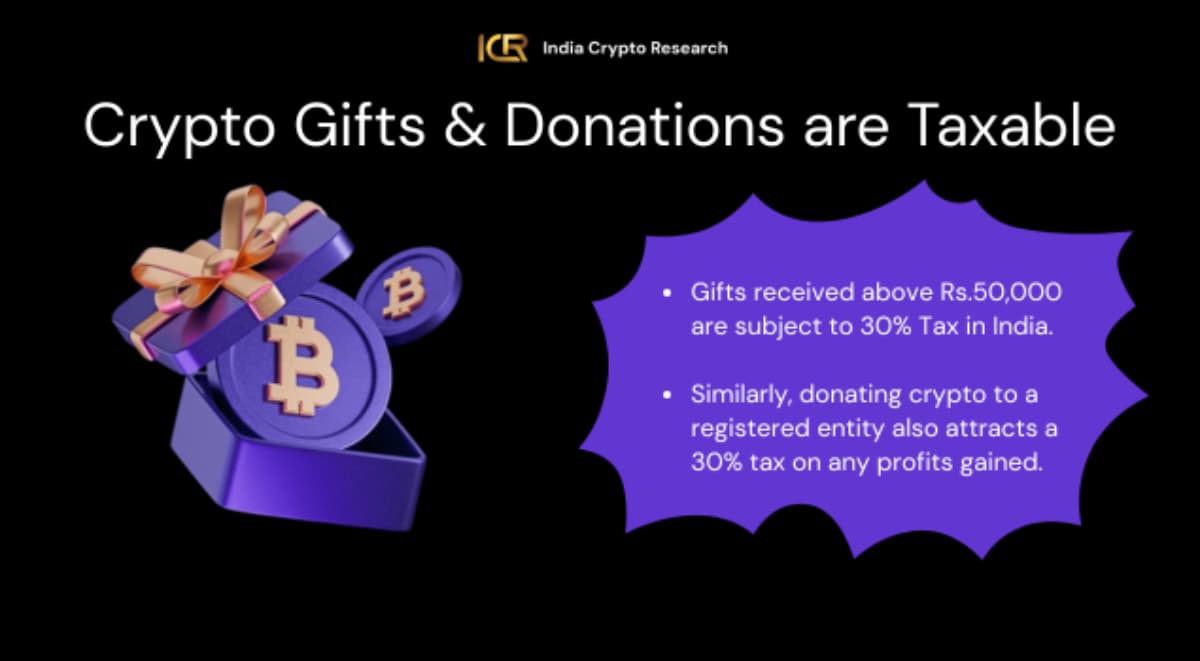

If you are a resident individual and you buy crypto, sell it, swap one crypto for another, or receive crypto in any form, you fall within the scope of crypto taxation. The frequency of activity does not matter. Even a single transaction can create a reporting obligation.

A common misunderstanding relates to holding. Many people believe tax applies only when crypto is converted into cash. In reality, tax responsibility can arise even when value moves from one crypto asset to another. The form of value changes, but the system still recognises that a transfer has taken place.

Timing also matters.

Tax responsibility arises at the moment a taxable action occurs. This includes:

It does not wait until the end of the financial year, and it does not depend on whether profits are withdrawn to a bank account.

This approach may feel strict, but it aligns with how the tax system views value creation. Once value is realised or received, it becomes reportable.

Understanding this early helps avoid one of the most common mistakes in crypto taxation. Leaving tax considerations until filing season often creates gaps that are difficult to correct later.

Crypto activity rarely stays confined to a single exchange or a single year. Trades, rewards, and transfers often span multiple platforms and financial years, which makes manual tax calculation error prone.

The ICR Crypto Tax Calculator is built to handle this reality.

Users can upload their trade history directly from supported crypto exchanges or connect their wallets to capture on chain activity. Once the data is imported, the system organises every transaction by financial year, rather than treating everything as a single pool of activity.

For each financial year, the calculator applies Indian crypto tax rules independently. This includes:

This year wise segregation is critical because tax treatment depends on when an activity occurred, not when it is remembered or reported.

At the end of the process, the tool generates a consolidated tax report. This report is structured to align with Indian filing requirements and can be shared directly with a Chartered Accountant for ITR filing. Instead of reconstructing history during filing season, the focus shifts to review and verification.

In practice, this approach mirrors how crypto compliance works best. Capture activity early, classify it correctly by year, and file with clarity.

Understanding what crypto is, how the Indian government recognises it, and why it is taxed helps remove much of the confusion that surrounds this space. The tax framework may feel unfamiliar, but its intent is clear. When value exists and changes hands, responsibility follows.

What matters most at this stage is recognising whether these rules apply to you. In India, crypto taxation is not based on labels or intentions. It is based on activity. Even limited participation can create reporting obligations.

Once this is understood, the conversation naturally shifts from whether crypto is taxed to how everyday crypto actions are treated under the law.

In the next part, we will break down which crypto actions attract tax in India, how different activities are viewed, and why understanding these triggers is critical for staying compliant.

India Crypto Research operates independently. The information presented herein is intended solely for educational and informational purposes and should not be construed as financial advice. Before making any financial decisions, it's essential to undertake your own thorough research and analysis. If you're uncertain about any financial matters, we strongly recommend seeking guidance from an impartial financial advisor.