Where the cost of sending money hides

What a stablecoin actually is

The payment giants have quietly picked a side

Every major economy has picked a side

The regulation gap India has to close

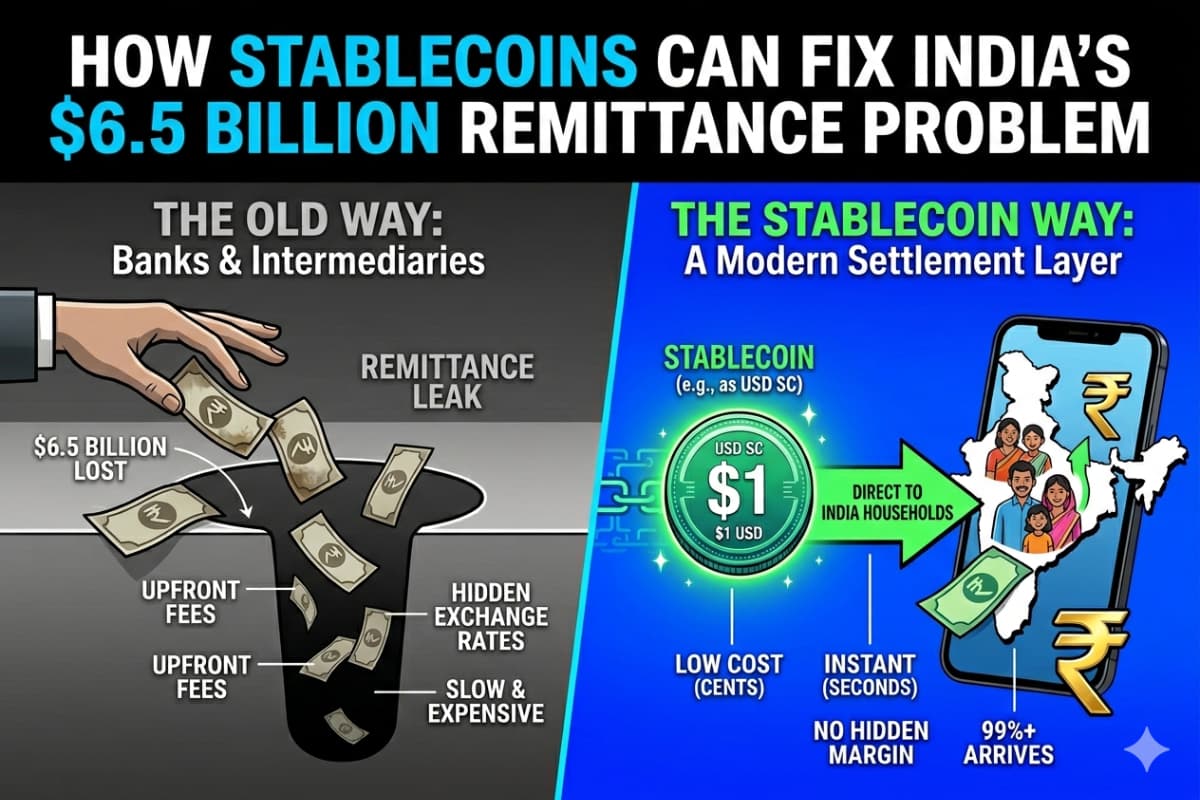

India received $135 billion in remittances in FY2024-25. No country has ever recorded a higher number. But about $6.5 billion of it never reached Indian households. Banks, money transfer operators, and other intermediaries took their cut before the transfer was completed. That one year of loss is more than 4 times ISRO's entire annual budget. It is enough to build 30 new AIIMS hospitals every year.

While this leak continues, a new system called stablecoins has been doing the same kind of work globally at a fraction of the cost. In the last 12 months, $13 trillion in value has moved through stablecoins. That is more than Mastercard and closing in on Visa's. India, despite being the world's largest receiver of cross-border money, has played no role in building the infrastructure that is starting to move it.

Indian households track most financial costs carefully. Home loan rates, FD yields, credit card cashback, and GST on a restaurant bill. Remittance fees do not get tracked the same way because they are harder to see.

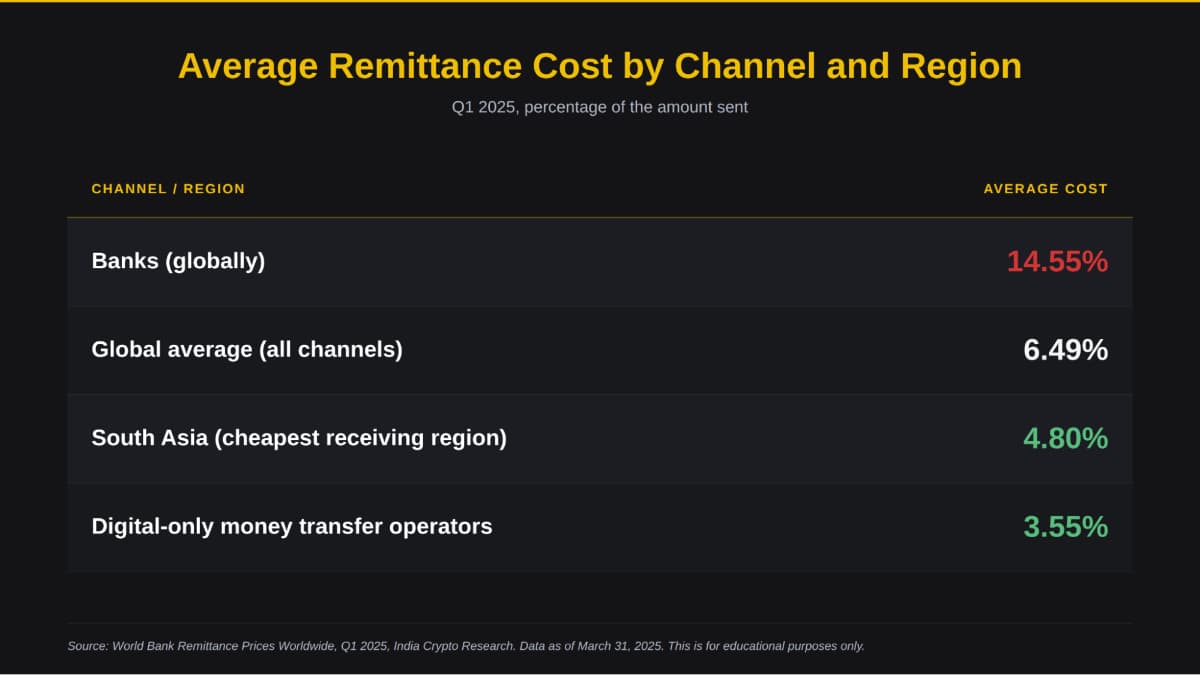

The World Bank measures every remittance in terms of two costs. One is the upfront transfer fee, which is shown to the sender. The other is the exchange rate margin, which is hidden inside the conversion rate. The bank or operator applies a rate that is usually 2 to 3% worse than the actual market rate. The sender never sees this part directly. Together, the two costs can range from under 1% to over 14% of the amount sent.

The World Bank's Q1 2025 data shows how wide the gap is between different channels. A 4.8% fee looks small on a single $1,000 transaction. Apply it to $135 billion of yearly inflows, and the picture changes completely. The result is roughly $6.5 billion of value lost before Indian families even touch the money. The bigger the inflow, the bigger the drain.

A stablecoin is a digital token whose value is fixed to a real currency, almost always the US dollar. Unlike Bitcoin or Ethereum, the price does not move. A dollar-pegged stablecoin worth $1 today is worth $1 tomorrow. The largest ones, USDT and USDC, are backed by short-term US Treasuries and cash held in separate reserves.

What makes a stablecoin different from a bank deposit is how it travels. Stablecoins live on public blockchains. A sender in New Jersey can transfer one to a wallet in Mumbai in under a minute. The fee is usually a few cents, regardless of the size of the transaction. No correspondent banks. No SWIFT messages. No hidden exchange rate margin.

The scale this has reached is the part most Indian readers underestimate. In the last 12 months, stablecoins moved roughly $13 trillion. Visa processed about $15 trillion in the same period. Mastercard processed about $10 trillion. Stablecoins, in Q1 2026, have already passed Mastercard and Visa.

These figures are not retail traders moving coins between exchanges. The numbers strip out bot activity and internal transfers. What is left is a real economic settlement.

The clearest sign that stablecoins are becoming payment infrastructure is what the incumbents are doing with them.

Stripe paid $1.1 billion in 2024 to buy Bridge, a company that builds stablecoin payment rails for businesses. Transaction volume through Bridge has grown fourfold in the year since. Stripe now lets merchants in over 100 countries accept stablecoin payments, with settlement happening on a public blockchain instead of through SWIFT.

Visa is doing the same thing one layer up. In December 2025, it launched stablecoin settlement for US banks on the Solana blockchain. By January 2026, the programme was running at an annualised $4.5 billion. Banks in the programme can now settle their Visa obligations in a dollar-pegged stablecoin, 7 days a week, weekends included.

PayPal launched its own dollar-pegged stablecoin, PYUSD, in 2023. Meta is preparing one for 2026. Every major payment company has now made a stablecoin commitment.

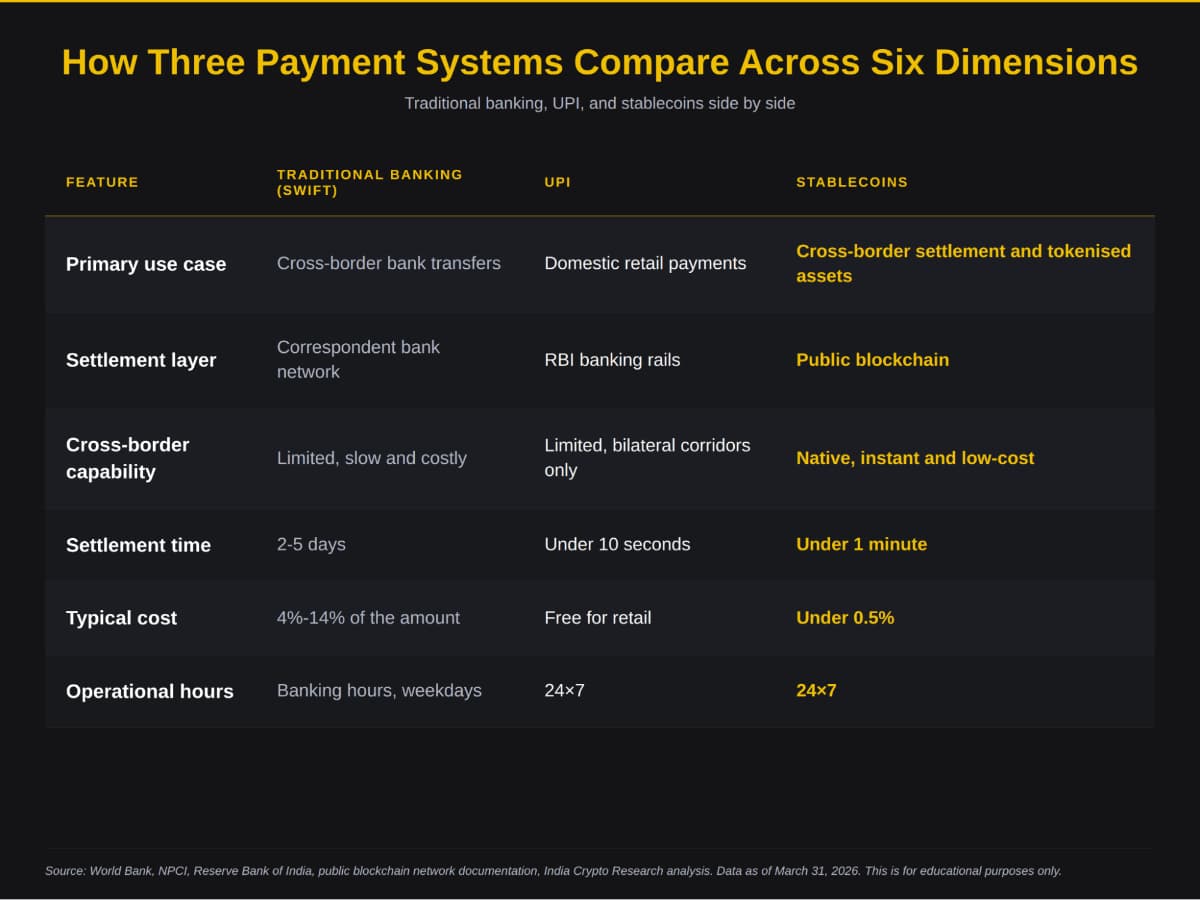

This is a fair question. India built UPI, the most advanced retail payment system in the world. Why can UPI not handle cross-border flows the same way it handles domestic ones?

UPI processes around 20 billion transactions every month in India. It is free for retail users, settles in under 10 seconds, and is built on public infrastructure that countries from Brazil to France are now copying. But UPI was designed for one specific job. Instant transfers between accounts inside the Indian banking system. Every bank, every payee, every transaction has to settle through RBI-governed rails.

India has tried to extend UPI internationally. The UPI-PayNow link with Singapore went live in 2023. In November 2025, the RBI and the European Central Bank announced a phased integration between UPI and TIPS, the Eurozone's instant payment system. UPI is now live for merchant payments in 8 countries, including the UAE, France, Mauritius, and Bhutan.

But these are bilateral corridors. Each one has to be negotiated country by country. Each takes years. And most of them are used by Indian travellers paying merchants abroad, not by NRIs sending money home.

Stablecoins work differently. They are not a national payment network plugging into other national payment networks. They are a global settlement layer that does not need permission from any banking system. A freelancer in Singapore paid in USDC by a US client receives the money in seconds and decides when, where, and how to convert it.

UPI and stablecoins are not competing systems. They sit on different layers of the financial stack and solve different problems. India has built one of these layers brilliantly. The other is being built without India in the room.

Stablecoin regulation has moved from theory to practice over the last 18 months, and India is the biggest country still on the sidelines.

The European Union's Markets in Crypto-Assets regulation, known as MiCA, became fully operational in December 2024. It gives stablecoin issuers a single licence that works across all 27 member states. The United States passed the GENIUS Act in 2025, creating a federal framework specifically for dollar-backed stablecoins. The UAE's Virtual Assets Regulatory Authority has published detailed rules covering issuance, custody, exchange, and advisory services. Japan licensed its first yen-backed stablecoin issuer in early 2025. South Korea, Singapore, and Hong Kong have all released their own frameworks.

India has one private piece in motion. In November 2025, Polygon Labs and an Indian fintech called Anq announced ARC, the first rupee-pegged stablecoin backed by Indian government securities. Launch is targeted for 2026. Polygon was founded by Indian entrepreneur Sandeep Nailwal. But ARC is one product. What India still lacks is the broader regulatory framework that the EU, US, and UAE have already built.

India has no specific regulation for stablecoins. They are treated under the broader Virtual Digital Asset framework introduced in the 2022 Finance Act. That framework was designed for cryptocurrency in general, not for payment instruments. Any gain on a stablecoin transaction is taxed at 30%. Every transfer attracts 1% TDS.

The 1% TDS is the most immediate blocker. A payment system cannot function when every transaction is taxed. If a freelancer receives $1,000 in stablecoins and pays a supplier with the same money the next week, the tax department takes 1% from each leg. This works for investing. It does not work for payments.

The bigger gaps sit further up. Stablecoins are not recognised as a payment instrument under India's Payment and Settlement Systems Act. The RBI has not allowed Indian banks to custody them or provide banking services to stablecoin issuers. FEMA does not specify how foreign-issued stablecoins should be treated when received as payment from abroad. The RBI has also been openly resistant, urging in its December 2025 Financial Stability Report that countries prioritise central bank digital currencies over privately issued ones.

A crypto regulation discussion paper has been worked on for over 2 years. As of April 2026, it had still not been released for public consultation. The EU took 3 years to draft MiCA. India has not completed even the first round.

The question is no longer whether India eventually permits stablecoins. It is whether India treats them as a payment problem that needs a framework, or as a sovereignty problem that needs to be contained. The first answer rebuilds India's claim on the $6.5 billion leaking out every year. The second concedes it permanently.

India Crypto Research operates independently. The information presented herein is intended solely for educational and informational purposes and should not be construed as financial advice. Before making any financial decisions, it's essential to undertake your own thorough research and analysis. If you're uncertain about any financial matters, we strongly recommend seeking guidance from an impartial financial advisor.